Jakarta, 9 January 2026 — The Monthly Board of Commissioners Meeting of the Indonesia Financial Services Authority (OJK), held on 24 December 2025, assessed that stability in the Financial Services Sector (SJK) remained well maintained.

Recent global economic data point to improving conditions, although China’s economic performance continues to fall short of expectations. Globally, manufacturing activity remains in expansionary territory, albeit moderating in line with declining consumer confidence. Looking ahead to 2026, various multilateral organisations project that global economic growth will continue to slow to below its pre-pandemic average, reflecting rising fiscal risks in several major economies.

In the United States, economic performance remained relatively solid. Gross domestic product (GDP) grew by 4.3 percent (SAAR) in the third quarter of 2025, accelerating from the previous quarter and exceeding market expectations. Growth was supported by household consumption, lower imports, and increased investment in artificial intelligence (AI). Meanwhile, the labour market showed early signs of moderation, with headline inflation easing to 2.7 percent in November 2025 and core inflation declining to 2.6 percent (October 2025: 3.0 percent).

In China, economic moderation persisted, with household consumption remaining subdued. On the supply side, the manufacturing Purchasing Managers’ Index (PMI) returned to contractionary territory, while pressures in the property sector continued.

These developments prompted several central banks to maintain accommodative monetary policy stances. The Federal Reserve (Fed) reduced the Federal Funds Rate (FFR) by 25 basis points at its December 2025 meeting. Similarly, the Bank of England (BoE) lowered its policy rate by 25 basis points to 3.75 percent, marking its fourth rate cut in 2025. In contrast, the Bank of Japan (BoJ) raised its policy rate to the highest level in more than three decades to curb persistent inflationary pressures.

Diverging monetary policy paths influenced global financial market dynamics. Global equity markets generally rallied following the FFR cut, despite concerns regarding a potential technology bubble. Meanwhile, Japan’s interest rate hike weighed on global sovereign bond markets amid the unwinding of carry trades. At the start of 2026, market participants also remained attentive to geopolitical developments in Venezuela and their potential implications for global financial markets and political stability.

Against this global backdrop, Indonesia’s domestic economy in 2025 recorded higher core inflation. Nevertheless, the manufacturing sector remained in expansionary territory, while external performance was sustained, as reflected in a continued trade surplus.

Developments in the Capital Market, Financial Derivatives, and Carbon Exchange Sector (PMDK)

Supported by resilient domestic economic performance and positive global financial market sentiment, Indonesia’s capital market closed 2025 on a solid footing. The Jakarta Composite Index (JCI) ended 31 December 2025 at 8,646.94, rising by 1.62 percent month-to-month (mtm) and 22.13 percent year-to-date (ytd). Throughout 2025, the JCI recorded 24 all-time highs, peaking at 8,710.70 on 8 December 2025, with market capitalisation reaching IDR16,005 trillion on the same day. Meanwhile, the LQ45 and IDX80 indices increased by 2.41 percent and 10.07 percent (ytd), respectively.

The average daily trading value reached an all-time high of IDR27.19 trillion in December 2025 and has consistently remained above IDR20 trillion since August 2025. Market liquidity strengthened during the second half of 2025, driven by the growing participation of domestic retail investors. The share of retail investor transactions increased from 38 percent in 2024 to 50 percent in 2025. Overall, average daily trading value rose to IDR18.07 trillion in 2025 from IDR12.85 trillion in 2024.

In line with improved market performance, non-resident investors recorded a net buy of IDR12.24 trillion (mtm) in December 2025, extending the buying momentum from the previous month. Increased non-resident inflows during the fourth quarter of 2025 reflect positive investor perceptions of and confidence in Indonesia’s financial markets and economic outlook. On an annual basis, however, non-resident investors posted a cumulative net sell of IDR17.34 trillion in 2025.

The bond market continued to strengthen in December 2025, with the Indonesia Composite Bond Index (ICBI) rising by 1.08 percent (mtm) and 12.27 percent year-on-year (yoy). Government securities (SBN) yields declined by an average of 4.84 basis points during the month, despite increasing by 80.91 basis points on an annual basis. Non-resident investors recorded a net inflow of IDR6.49 trillion (mtm) into the SBN market in December 2025 (yoy: net buy of IDR2.01 trillion). In the corporate bond market, non-resident investors posted a net buy of IDR0.21 trillion (mtm), compared with a net sell of IDR1.39 trillion (yoy).

In the investment management industry, assets under management (AUM) reached IDR1,033.81 trillion at the end of December 2025, increasing by 3.08 percent (mtm) and 23.46 percent (yoy). Net asset value (NAV) of mutual funds stood at IDR675.32 trillion, up 4.80 percent (mtm) and 35.26 percent (yoy), supported by net subscriptions of IDR23.91 trillion (mtm) and IDR138.69 trillion (yoy).

During December 2025, 694 thousand new investors entered the capital market. Over the course of 2025, the total number of capital market investors increased by 5.49 million to 20.36 million, representing growth of 36.95 percent (yoy).

Capital market fundraising remained robust, with the 2025 target of IDR220 trillion successfully exceeded. Total public offering value reached IDR274.80 trillion, including 20 new issuers that raised IDR16.21 trillion. In addition, 29 public offering pipelines remain active, with an indicative value of IDR22.28 trillion.

In securities crowdfunding (SCF), 27 new securities were issued in December 2025, raising IDR44.18 billion from 12 new issuers. Cumulatively, 978 securities issuances were completed by 585 issuers, involving 191,981 investors and total funds raised of IDR1.82 trillion.

In the financial derivatives market, from 10 January to the end of 2025, OJK granted principal licences to 113 entities, comprising four futures exchanges, 23 Alternative Trading System (Sistem Perdagangan Alternatif/SPA) traders, 63 futures brokers, 15 margin deposit banks, six futures advisers, one association, and one professional certification institution. In December 2025, total transaction volume reached 61,613 lots, bringing the annual total to 1,013,294 lots. Transaction frequency increased by 239,850 during the month, resulting in total annual frequency of 4,433,781 transactions.

From its launch on 26 September 2023 through 30 December 2025, the carbon exchange registered 150 service users. In December 2025, transaction volume increased by 190,264 tCO2e, bringing cumulative volume to 1,811,933 tCO2e, with an accumulated transaction value of IDR87.00 billion.

Enforcement of PMDK Regulations

- In December 2025, OJK imposed administrative sanctions in the form of fines totalling IDR52.81 billion on 52 entities for violations of prevailing PMDK regulations, along with three written warnings.

- Throughout 2025, OJK imposed administrative sanctions following capital market investigations, including fines totalling IDR80.75 billion on 121 entities, revocation of individual licences for six entities, written warnings to 42 entities, and five written reprimands.

- OJK also imposed administrative fines totalling IDR50.38 billion on 638 financial services institutions (PUJK) in the capital market for regulatory violations, in addition to issuing 219 written warnings for late submission of reports. Furthermore, fines amounting to IDR300 million and 62 written warnings were imposed for other non-case violations, excluding late submissions.

Developments in the Banking Sector (PBKN)

Banking intermediation accelerated in the reporting period with a well-managed risk profile and ample liquidity. In November 2025, credit grew by 7.74 percent (yoy) (October 2025: 7.36 percent) to IDR8,314.48 trillion, primarily driven by growth in the transportation and storage sector (18.33 percent), electricity, gas, and water supply (21.83 percent), the mining industry (11.0 percent), and construction (8.14 percent).

Intermediation performance at the end of 2025 is projected to strengthen, with credit growth forecast to be above the lower end of the OJK target and third-party funds (TPF) to grow by double digits. Such conditions indicate that the banking industry has successfully overcome various challenges in loan disbursement, and the real sector is showing early signs of improving demand. In 2026, banking performance is projected to remain solid, with stable credit and TPF growth supported by maintained credit quality and substantial capital.

By loan type, investment loans posted the strongest growth at 17.98 percent, primarily supported by the mining sector and manufacturing industry. Investment loan growth in 2025 was the highest recorded over the past decade, demonstrating the banking industry's role in financing expansion and increasing the real sector's capacity to bolster long-term growth. Meanwhile, consumer loans posted 6.67 percent (yoy) growth, and working capital loans increased by 2.04 percent (yoy). Based on borrower segment, corporate loans posted 12.06 percent growth, while MSME loans contracted by 0.64 percent (yoy).

Meanwhile, third-party funds (TPF) maintained high growth of 12.03 percent (yoy) in the reporting period (October 2025: 11.48 percent yoy), reaching IDR9,899.07 trillion. The banking industry continued to lower deposit rates. Relative to the previous year, the weighted-average interest rate on rupiah loans fell by 26 bps (yoy) and 4 bps (mtm) to 8.97 percent in November 2025 (November 2024: 9.23 percent, October 2025: 9.01 percent), primarily driven by interest rates on productive loans. Interest rates on working capital loans decreased by 44 bps (yoy) and 6 bps (mtm) to 8.24 percent in November 2025 (November 2024: 8.68 percent, October 2025: 8.30 percent).

Regarding fund mobilisation, the weighted-average rupiah deposit rate decreased by 29 bps and 8 bps (mtm) to 2.77 percent in November 2025 (November 2024: 3.06 percent; October 2025: 2.85 percent), with declines predominantly in term deposits. The interest rate on term deposits fell 66 bps (yoy) and 15 bps (mtm) to 4.60 percent in November 2025 (November 2024: 5.26 percent, October 2025: 4.75 percent).

Liquidity in the banking industry remained ample in November 2025, with the ratios of liquid assets to non-core deposits (LA/NCD) and liquid assets to third-party funds (LA/TPF) recorded at 131.49 percent (October 2025: 130.97 percent) and 29.77 percent (October 2025: 29.47 percent), respectively, well above the regulatory thresholds of 50 percent and 10 percent. Meanwhile, the Liquidity Coverage Ratio (LCR) was recorded at 210.38 percent, and the loan-to-deposit ratio (LDR) stood at 83.99 percent, both considered adequate in anticipation of increased loan disbursements.

Meanwhile, credit quality in the banking industry remained stable, as indicated by gross NPL ratios of 2.21 percent (October 2025: 2.25 percent) and net NPL ratios of 0.86 percent (October 2025: 0.90 percent). Loans at Risk (LaR) decreased from the previous period to 9.22 percent (October 2025: 9.41 percent).

Banking industry resilience also remained solid, as reflected in a high Capital Adequacy Ratio (CAR) of 26.05 percent (October 2025: 26.38 percent), providing a robust buffer against global uncertainty.

The share of Buy Now Pay Later (BNPL) loans disbursed by the banking industry stood at just 0.32 percent of total credit, but continues to record strong annual growth. As of November 2025, the balance of outstanding BNPL loans reported via the Financial Information Services System (SLIK) grew by 20.34 percent (yoy) (October 2025: 21.03 percent yoy) to IDR26.20 trillion (October 2025: IDR25.72 trillion), with the number of accounts increasing to 31.47 million (October 2025: 30.99 million) and a gross NPL ratio of 2.04 percent (October 2025: 2.50 percent).

Seeking to enforce regulations and protect consumers in the banking industry, OJK revoked the business licence of PT BPR Bumi Pendawa Raharja, located in Cianjur, West Java, on 15 December 2025. Regarding the ongoing crackdown on online gambling, which has wide-reaching and deleterious impacts on the economy and financial sector, OJK has instructed banks to block approximately 31,382 accounts (previously 30,392) based on data submitted by the Ministry of Communication and Digital Affairs. In addition, OJK is following up on the reports by requesting that banks close accounts associated with specific Population Identification Numbers (NIKs) and mandating Enhanced Due Diligence (EDD).

Developments in the Insurance, Guarantee, and Pension Fund Industry (PPDP)

Overall performance of the PPDP industry remained stable, supported by strong aggregate solvency levels. OJK continues to optimise industry functions and performance by strengthening resilience amid evolving global and domestic economic dynamics.

As of November 2025, total insurance industry assets amounted to IDR1,194.06 trillion, reflecting growth of 5.96 percent (yoy). Within the commercial insurance segment, total assets reached IDR971.22 trillion, increasing by 7.49 percent (yoy).

From January to November 2025, premium income in the commercial insurance industry totalled IDR297.88 trillion, representing growth of 0.41 percent (yoy). This comprised life insurance premiums, which declined by 0.75 percent (yoy) to IDR163.88 trillion, and general insurance and reinsurance premiums, which grew by 1.88 percent (yoy) to IDR134.00 trillion.

Capitalisation in the commercial insurance industry remained strong, with aggregate risk-based capital (RBC) ratios of 488.69 percent for life insurance and 342.88 percent for general insurance and reinsurance—well above the minimum regulatory requirement of 120 percent.

For non-commercial insurance, which includes BPJS Ketenagakerjaan, BPJS Kesehatan, and insurance programmes for civil servants (ASN), military personnel (TNI), and police personnel (POLRI) related to work accident and death benefits, total assets reached IDR222.84 trillion, growing by 0.23 percent (yoy).

The pension fund industry also recorded solid growth. As of November 2025, total pension fund assets increased by 10.72 percent (yoy) to IDR1,662.16 trillion. Assets under voluntary pension programmes grew by 6.81 percent (yoy) to IDR405.20 trillion.

Meanwhile, compulsory pension programmes—including old-age and pension benefits managed by BPJS Ketenagakerjaan, as well as retirement savings and pension contribution schemes for ASN, TNI, and POLRI—recorded total assets of IDR1,256.95 trillion, reflecting growth of 12.04 percent (yoy).

In the guarantee sector, total assets reached IDR47.63 trillion as of November 2025, increasing by 2.03 percent (yoy).

Regarding regulatory enforcement and consumer protection in the PPDP sector, OJK undertook the following actions:

- Implemented the first phase of equity enhancement obligations for 2026 in accordance with OJK Regulation (POJK) Number 23 of 2023. Based on monthly reports as of October 2025, 115 out of 144 insurance and reinsurance companies (79.86 percent) have fulfilled the minimum equity requirements for 2026.

- Continued efforts to resolve issues affecting financial services institutions (FSIs) through special surveillance measures. As of 22 December 2025, six insurance and reinsurance companies and seven pension funds were placed under special surveillance to improve their financial condition in the interest of policyholders and participants.

Developments in Financing Institutions, Venture Capital Firms, Microfinance Institutions, and Other Financial Service Institutions Sector (PVML)

In the PVML sector, financing receivables of finance companies (PP) grew by 1.09 percent (yoy) in November 2025 (October 2025: 0.68 percent yoy), totalling IDR94.85 trillion506.82 trillion. This growth was underpinned by working capital financing, which expanded by 8.99 percent (yoy).

Finance companies continued to manage their risk profiles effectively, as reflected in gross and net non-performing financing (NPF) ratios of 2.44 percent and 0.85 percent, respectively (October 2025: 2.83 percent and 0.83 percent). The gearing ratio stood at 2.13x (October 2025: 2.15x), remaining well below the regulatory cap of 10x.

Venture capital financing recorded growth of 1.20 percent (yoy) in November 2025 (October 2025: -0.10 percent yoy), reaching IDR16.29 trillion.

In the FinTech peer-to-peer (P2P) lending industry, outstanding financing increased by 25.45 percent (yoy) in November 2025 (October 2025: 23.86 percent yoy), totalling IDR94.85 trillion. The aggregate credit risk level (TWP90) was recorded at 4.33 percent (October 2025: 2.76 percent).

Financing disbursed by the pawnbroking industry grew by 42.88 percent (yoy) in November 2025 (October 2025: 38.89 percent yoy), reaching IDR125.44 trillion, while credit risk remained well contained. Pawn products remained the primary driver, accounting for IDR102.75 trillion, or 81.92 percent, of total financing disbursed.

Based on data from the Financial Information Services System (SLIK), Buy Now Pay Later (BNPL) financing disbursed by finance companies increased by 68.61 percent (yoy) in November 2025 (October 2025: 69.71 percent yoy) to IDR11.24 trillion, with a gross NPF ratio of 2.78 percent (October 2025: 2.79 percent).

Regarding regulatory enforcement and consumer protection in the PVML sector, OJK undertook the following measures:

- Capital adequacy compliance: Four out of 145 finance companies had yet to comply with the minimum equity requirement of IDR100 billion, while nine out of 95 P2P lenders had not met the minimum equity requirement of IDR12.5 billion. All affected P2P lenders have submitted action plans to OJK, outlining steps to meet the requirements, including capital injections from existing shareholders, the entry of strategic investors, and/or mergers with other P2P lenders.

- Compliance and integrity enforcement: In December 2025, OJK imposed administrative sanctions on 24 finance companies, six venture capital firms, 23 P2P lenders, four microfinance institutions, 13 private pawnbrokers, and one specialised financial institution for violations of prevailing POJK regulations and/or findings from supervisory activities and follow-up examinations. The sanctions comprised 52 fines and 146 written warnings.

OJK expects these enforcement measures to strengthen governance, prudence, and regulatory compliance in the PVML sector, thereby improving overall performance and optimising the sector’s contribution to the economy.

Developments in Financial Sector Technology Innovation, Digital Financial Assets, and Crypto Assets Sector (IAKD)

1. Regulatory Sandbox Implementation

- Following the promulgation of POJK No. 3/2024 on Financial System Technology Innovation (ITSK), interest among ITSK providers in participating in OJK’s regulatory sandbox remains strong. As of December 2025, OJK had received 303 consultation requests from prospective sandbox participants.

- OJK received 26 sandbox applications, of which eight were approved. Approved participants include:

- Four ITSK providers with Digital Financial Asset and Crypto Asset (AKD-AK) business models, currently undergoing trials; and

- Four ITSK providers that successfully completed the sandbox process and obtained “Pass” status, namely:

- PT Indonesia Blockchain Persada (Blocktogo) – approved on 8 August 2025, with a gold tokenisation business model (AKD-AK) through the Gold Indonesia Republic (GIDR) product;

- PT Sejahtera Bersama Nano – approved on 8 October 2025, implementing a securities tokenisation model based on the Fund Management Contract (KPD) scheme;

- PT Teknologi Gotong Royong (GORO) – approved on 5 November 2025, operating a property ownership tokenisation model and functioning as a digital financial asset trading platform; and

- PT Properti Gotong Royong – approved on 5 November 2025, acting as the property owner and custodian for assets tokenised and traded on the GORO platform.

In accordance with POJK 3/2024 on Financial System Technology Innovation (ITSK), PT Indonesia Blockchain Persada, PT Sejahtera Bersama Nano, and PT Teknologi Gotong Royong may register with OJK. Furthermore, ITSK providers with the same business model as PT Indonesia Blockchain Persada, PT Sejahtera Bersama Nano, or PT Teknologi Gotong Royong now have the same rights to register with OJK without completing the sandbox process.

c. Seven applications to become sandbox participants are currently under review by OJK for providers with the AKD-AK business model.

2. ITSK provider licensing:

- As of December 2025, a total of 30 official ITSK providers were registered with OJK, consisting of ten Innovative Credit Scoring (ICS) providers and 20 Financial Service Aggregators (PAJK). Given the completion of the registration process for all ITSK providers based on the ICS and PAJK business models, in accordance with POJK 3/2024 concerning Financial System Technology Innovation (ITSK), registered ITSK providers are required to submit license applications to OJK. Meanwhile, new prospective ICS and PAJK providers can apply directly to OJK for a business license.

- As of December 2025, OJK received 23 license applications from ITSK providers, including nine ICS providers and 14 PAJK aggregators, which are currently under review by OJK. In accordance with POJK No. 3/2024, PT Indonesia Blockchain Persada, PT Sejahtera Bersama Nano, and PT Teknologi Gotong Royong are eligible to proceed directly with registration at OJK. ITSK providers with identical business models are likewise permitted to register without undergoing the sandbox process.

- Seven additional sandbox applications for AKD-AK business models are currently under review.

2. Licensing of ITSK Providers

- As of December 2025, 30 ITSK providers were officially registered with OJK, comprising ten Innovative Credit Scoring (ICS) providers and 20 Financial Service Aggregators (PAJK). In line with POJK No. 3/2024, all registered providers under these models are required to apply for a business licence. New prospective ICS and PAJK providers may apply directly for licensing.

- OJK had received 23 license applications as of December 2025, consisting of nine ICS providers and 14 PAJK providers, all of which are currently under review.

Based on reports submitted as of November 2025, registered ITSK providers have established 1,317 partnerships with financial service institutions across banking, finance companies, insurance, securities, P2P lending, microfinance institutions, and pawnbrokers, as well as with IT service and data providers.

During November 2025, PAJK facilitated partner-approved transactions amounting to IDR2.23 trillion, bringing the year-to-date total for 2025 to IDR24.11 trillion, with 16.01 million users nationwide. Meanwhile, ICS providers recorded 17.83 million credit score inquiries during the reporting period, bringing the 2025 year-to-date total to 170.72 million. These developments highlight the significant role of ITSK providers in accelerating financial market deepening, accessibility, and inclusion.

Crypto Asset Developments

As of December 2025, 1,373 crypto assets were listed as tradeable in Indonesia. OJK had licensed 29 entities in the crypto ecosystem, comprising one exchange, one clearing and settlement institution, two custodians, and 25 crypto asset traders (PAKD). In addition, seven supporting institutions were approved, including five Payment Service Providers (PSPs) and two custodian banks (BPDKs).

OJK is currently reviewing applications from prospective crypto market participants, including two exchanges, two clearing institutions, two custodians, four CPAKD entities, and two PSPs.

The number of crypto asset consumers increased to 19.56 million in November 2025 (October 2025: 19.08 million). Transaction value in December 2025 amounted to IDR32.68 trillion, declining by 12.22 percent from November 2025, while the 2025 year-to-date transaction value reached IDR482.23 trillion, indicating sustained consumer confidence and stable market conditions.

Digital Innovation and Enforcement

To promote digital financial innovation with tangible impact on the real sector, particularly the creative economy, OJK’s Innovation Centre (OJK Infinity), in collaboration with the Ministry of the Creative Economy, organised the OJK–Ekraf Hackathon 2025 from 8 October to 15 November 2025. The event attracted 737 participants, resulting in 121 proposals, with three winners announced via the official platform.

From January to December 2025, OJK imposed administrative sanctions on 13 ITSK providers and 30 AKD-AK providers, consisting of 33 fines totalling IDR845 million and 37 written warnings. OJK expects these measures to reinforce governance, prudence, and regulatory compliance within the IAKD sector.

Developments in Market Conduct Supervision, Education and Consumer Protection Sector (PEPK)

From 1 January to 31 December 2025, OJK conducted 6,548 financial education activities, engaging more than 9.94 million participants nationwide. The Sikapi Uangmu platform published 340 educational contents, reaching 3.47 million viewers, while the Financial Education Learning Management System (LMSKU) recorded 43,635 users, 30,395 module accesses, and 18,249 completion certificates issued.

Under the GENCARKAN program, OJK organised 58,637 initiatives, comprising 37,203 educational activities and 21,434 digital education contents, covering 98.05 percent of Indonesia’s regencies and cities. These efforts were reinforced through collaboration with Regional Financial Access Acceleration Teams (TPAKD) across all provinces and regencies/cities.

Key Initiatives in December 2025, OJK implemented several strategic initiatives, including:

- Seeking to measure the financial literacy and inclusion index of Indonesian citizens at a more granular level, OJK in synergy with the Indonesia Deposit Insurance Corporation (LPS) and BPS-Statistics Indonesia committed to implement the National Financial Literacy and Inclusion Survey (SNLIK) 2026, with estimated coverage drilled down to the provincial level, through the signing of a SNLIK 2026 Implementation Cooperation Agreement on Wednesday, 17 December 2025.

- In collaboration with the Ministry of Social Affairs of the Republic of Indonesia, National Development Planning Agency, and National Disability Commission of the Republic of Indonesia, OJK launched Financial Literacy Guidelines for People with Disabilities, entitled Financially Smart and Healthy People with Disabilities towards Golden Indonesia 2045. The guidelines were launched on 8 December 2025 in Jakarta, coinciding with National Disability Day. The event also provided financial education activities, attended by 500 participants, including 300 people living with a disability and 200 carers.

- In synergy with the Ministry of Primary and Middle Education as well as educators, OJK implemented a pilot project to introduce financial literacy teaching materials at SMAN 74 Jakarta and SMKN 2 Jakarta. The activity integrated financial literacy materials into student learning sessions across various subjects, including mathematics to analyse financial spending patterns, economics to provide informative materials on financial products and financial institutions, and financial project management for school committee activities.

- Together with the Coordinating Ministry for Human Development and Cultural Affairs of the Republic of Indonesia, OJK hosted financial education activities on Mother's Day, entitled Financial Planning for Women: Women Plan, Women Invest, on 22 December 2025 in Jakarta. The hybrid educational activities engaged 480 participants, including 80 female employees from the Coordinating Ministry for Human Development and Cultural Affairs, as well as other relevant government ministries/agencies, in person, alongside 400 women participating online.

- Regional Financial Access Acceleration Teams (TPAKD) from various regions hosted Regional Coordination Meetings (Rakorda) alongside coaching clinics to build the capacity of their members. In December, such activities were implemented by the TPAKD in Yogyakarta on 4 December 2025, the TPAKD in Riau Islands on 9 December 2025, the TPAKD in West Java on 10 December 2025, the TPAKD in East Java on 16 December 2025, as well as the TPAKD in the Ex-Pekalongan Residency and the TPAKD in Lampung on 17 December 2025. The program was attended by Regional Heads and Regional Apparatus Organisations (OPD) in each region. During the Regional Coordination Meetings, the TPAKD Roadmap 2026-2030 was socialised, along with materials concerning the Regional Financial Access Index (IKAD) and a refreshment course on reporting through the SiTPAKD system.

- OJK Mass Media Appreciation 2025 served as a platform for OJK to express appreciation to its media partners for their meaningful contributions to OJK task implementation in 2025. At the event, OJK also implemented two special programs involving the broad participation of national and regional journalists, namely: (i) the Mass Media Journalist Article Writing Competition, with national and regional journalists competing to author articles that increase financial literacy, broaden public insight and raise strategic financial services sector issues, and (ii) selection of Best Mass Media Financial Literacy Ambassador, awarded to mass media journalists with strong dedication to producing educational content, building public understanding and serving as a role model for responsible reporting on the financial services sector. Both programs helped reinforce the message that the media not only delivers information but also stands at the forefront as a driver of national financial literacy.

- OJK was awarded the title of Best National Informative Public Agency and also received the Arkaya Wiwarta Prajanugraha Award from the Central Information Commission of the Republic of Indonesia (KIP) at the Public Information Disclosure Awards 2025. KIP presented the Arkaya Wiwarta Prajanugraha Award to OJK following a series of assessments involving seven types of public agencies: Government Ministries, State Institutions/Non-Ministerial Government Institutions (LN/LPNK), Universities, Provincial Governments, State-Owned Enterprises (BUMN), Non-Structural Institutions, and Political Parties. In addition to the Best National Informative Public Agency predicate, OJK was also recognised in second place as the Best Informative Public Agency in the State Institutions/Non-Ministerial Government Institutions (LN/LPNK) category. Informative Public Agency is the highest title for a public agency in terms of public information disclosure. This national award recognises OJK's commitment to prioritising transparency when disclosing information to the public, centrally and regionally.

- OJK received a Big 40 Award in the Consumer Protection Governance Strategist category from Business Indonesia as a form of appreciation for OJK's commitment and consistency to strengthening consumer protection governance, increasing financial literacy and education, as well as creating an ethical financial services sector in the public interest.

Consumer Services and Illegal Activity Eradication: Between 1 January and 28 December 2025, OJK received 536,267 consumer service requests, including 56,620 complaints, primarily related to banking, FinTech, and finance companies.

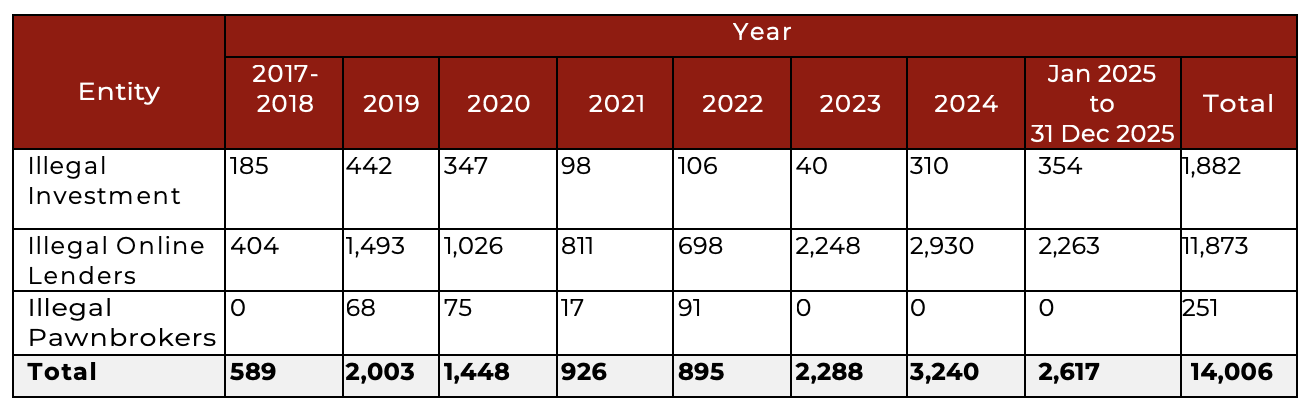

To combat illegal financial activities, OJK received 26,220 complaints in 2025, consisting of 21,249 cases related to illegal online lending and 4,971 cases involving illegal investment activities.

The number of illegal entities shut down/blocked is recapitulated as follows:

Enforcement of Consumer and Public Protection Regulations

Through the Task Force for the Eradication of Illegal Financial Activities (Satgas PASTI), OJK strengthened the enforcement of consumer and public protection regulations during the period January–31 December 2025, with the following outcomes:

- Eradication of illegal financial activities: OJK identified and shut down 2,263 illegal online lending entities and 354 illegal investment offerings operating across various websites and applications that posed potential harm to the public.

- Blocking of illegal debt collection and scam contacts: OJK identified contact numbers used by debt collectors affiliated with illegal online lending entities and coordinated with the Ministry of Communication and Digital Affairs of the Republic of Indonesia to block 2,422 contact numbers. In addition, Satgas PASTI monitored scam and fraud reports through the Indonesia Anti-Scam Centre (IASC) and identified 61,341 contact numbers reported by scam victims between November 2024 and 30 November 2025. Follow-up coordination with the Ministry resulted in the blocking of these reported contact numbers.

Indonesia Anti-Scam Centre (IASC)

Since its launch in November 2024 through 23 December 2025, IASC received 411,055 reports, comprising 218,665 reports submitted by victims via financial sector entities (banks and payment system operators) and subsequently handled through the IASC system, as well as 190,390 reports submitted directly by victims to IASC.

In total, 681,890 accounts were reported, of which 127,047 accounts were successfully blocked. Reported financial losses amounted to IDR9 trillion, with IDR402.5 billion in victim funds blocked. During the same period, 193 Financial Service Providers (FSPs) were reported. IASC will continue to enhance its operational capacity to accelerate the handling of fraud and scam cases in the financial services sector.

Enforcement of Consumer Protection Regulations

In enforcing consumer protection regulations during the period 1 January to 31 December 2025, OJK imposed the following sanctions:

- 175 written warnings issued to 144 FSPs;

- 40 written instructions issued to 40 FSPs; and

- 43 administrative fines imposed on 40 FSPs.

In addition, between 1 January and 14 December 2025, 177 FSPs were required to compensate consumer losses totalling IDR82.46 billion, USD3,281, and SGD27,365.

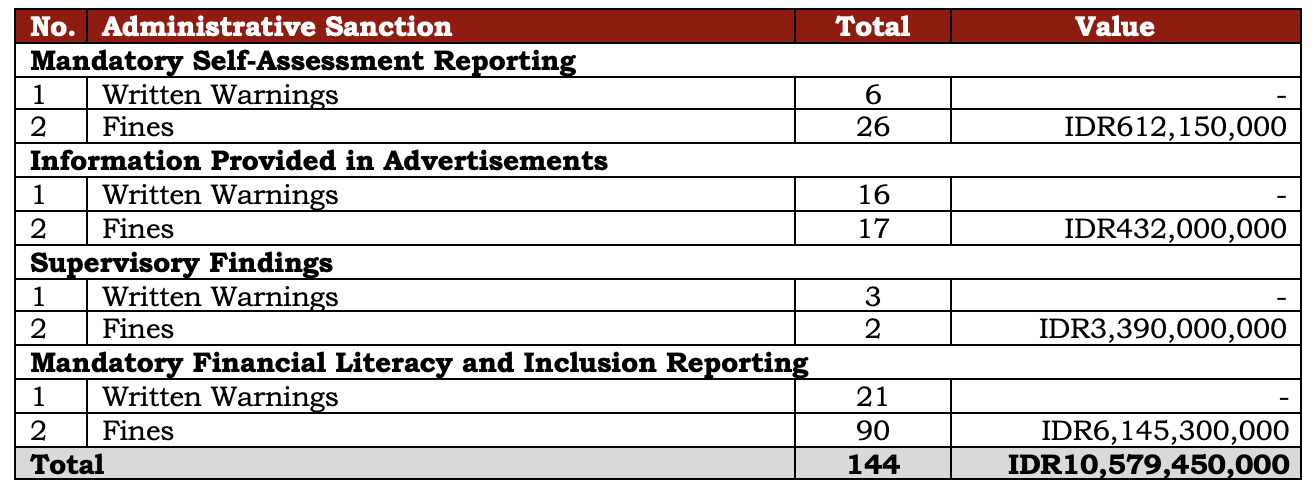

Enforcement of Self-Assessment Reporting Obligations

To enforce compliance with the mandatory submission of self-assessment reports for 2024 and 2025, OJK imposed:

- Six administrative sanctions in the form of written warnings; and

- Twenty-six administrative fines, amounting to IDR612.15 million.

These sanctions were imposed for late submission, failure to submit, and continued non-submission despite prior notifications. Financial Service Providers that failed to submit self-assessment reports remain obligated to do so in accordance with POJK No. 22/2023.

Market Conduct Supervision

In overseeing market conduct, OJK enforced regulations through administrative sanctions based on the results of on-site and off-site supervision. From 1 January to 31 December 2025, OJK imposed:

- 19 written warnings; and

- 17 administrative fines, totalling IDR3.82 billion,

for non-compliance with consumer protection provisions relating to advertising disclosures, debt collection practices, and insurance claims handling.

To prevent recurrence of similar violations, OJK also issued directives for corrective actions, including the removal of non-compliant advertisements, revisions to internal policies, and the settlement of consumer claims. These measures were implemented as part of supervisory coaching efforts to ensure sustained compliance with consumer and public protection regulations.

Enforcement of Financial Literacy and Inclusion Reporting

OJK also enforced compliance with the mandatory submission of financial literacy and inclusion reports in accordance with POJK No. 22/2023 on Consumer and Public Protection in the Financial Services Sector. Administrative sanctions were imposed for late submission or failure to submit:

- the financial literacy and inclusion plan for the second semester of 2024;

- the financial literacy and inclusion plan for 2025; and

- the financial literacy and inclusion realisation report for the first semester of 2025.

As of 31 December 2025, OJK had imposed 111 administrative sanctions, and comprising 21 written warnings, as well as 90 fines totalling IDR6.1 billion.

Between 1 January and 31 December 2025, therefore, OJK imposed the following sanctions:

OJK Policy Direction

To maintain financial system stability and expand the role of the financial services sector in supporting national economic growth, OJK implemented the following policy measures:

A. Policies to Maintain Financial System Stability

Despite the outlook for flatter global growth in 2026 and economic moderation in China, the performance of Indonesia’s financial services sector is expected to remain stable. To foster stronger and more resilient economic growth, OJK has implemented a range of strengthening measures, including within the PPDP industry. These measures include maintaining and refining regulatory frameworks for insurance companies, guarantee institutions, and pension funds, as well as strengthening the health insurance ecosystem to ensure insurers possess adequate digital capabilities and medical infrastructure.

In addition, OJK established a specialised unit—the Department of Islamic Finance and MSME Regulation and Development—to support MSME development and the advancement of sharia finance. This initiative aims to enhance MSME access to inclusive financing while fostering a fully integrated Islamic finance ecosystem encompassing Islamic banking, Islamic non-bank financial institutions, and the Islamic capital market.

B. Policies to Develop and Strengthen the Financial Services Sector and Market Infrastructure

1. Strengthening Market Infrastructure and Registration Processes

In collaboration with the Indonesian Central Securities Depository (KSEI), OJK integrated the OJK Integrated Registration and Licensing Information System (SPRINT) with the KSEI Electronic Securities Registration System (SPEK). This integration streamlines the registration process, strengthens regulatory assurance, and enhances governance in mutual fund product registration. The integration significantly accelerates and simplifies the investment management registration process by eliminating duplicate submissions and improving workflow efficiency.

2. Promulgation and Finalisation of Regulatory Frameworks

During the reporting period, OJK finalised and/or issued the following regulations:

- POJK No. 30/2025 on Governance and Risk Management for Financial System Technology Innovation (ITSK) Providers, establishing requirements for sound governance and proportionate risk management to ensure a sustainable ITSK ecosystem and support financial inclusion.

- POJK No. 31/2025 on Governance of Stock Exchanges, Clearing and Guarantee Institutions, and Depository and Settlement Institutions, strengthening governance among self-regulatory organisations (SROs) in line with the mandate of the Financial Sector Development and Strengthening Act (P2SK Act), including enhanced anti-fraud frameworks.

- POJK No. 32/2025 on Buy Now, Pay Later (BNPL), applicable to commercial banks and finance companies, governing prudential standards, consumer protection, cooperation mechanisms, information disclosure, and BNPL termination.

- POJK No. 33/2025 on Soundness Assessments for Insurance Companies, Guarantee Institutions, and Pension Funds, amending POJK No. 28/2020 to include guarantee institutions, expand risk coverage, and incorporate financial soundness ratios. This regulation is effective from 1 January 2026.

- POJK No. 34/2025 on Information Technology Implementation by Rural Banks and Sharia Rural Banks (BPR/BPRS), strengthening IT governance, risk management, cyber security, and resilience in line with growing digitalisation. This regulation amends POJK No. 75/POJK.03/2016.

- POJK No. 35/2025, amending POJK No. 46/2024 on the Development and Strengthening of Finance Companies, Infrastructure Financing Companies, and Venture Capital Firms, introducing deregulatory measures including:

- Motor vehicle down payments of up to 0 percent for eligible finance companies;

- Reduction of the Core Capital to Paid-Up Capital ratio from 150 percent to 50 percent for certain financing facilities; and

- Collateral exemptions for MSME working capital financing up to IDR100 million for eligible finance companies.

- POJK 36/2025 concerning Strengthening the Health Insurance Ecosystem, as a more strategic regulation than the previous rules concerning the implementation of health insurance products, as regulated by Circular Letter (SEOJK) Number 7/2025. The primary substance of this POJK includes obligations for insurance companies offering health insurance products to maintain adequate digital, medical, and Medical Advisory Board capabilities, as well as the obligation for insurance companies to review utilisation in the context of controlling costs and monitoring the quality of health services. In addition, the coordination mechanism among guarantee providers are regulated, along with each party's roles within the health insurance ecosystem, and health facilities are encouraged to provide healthcare services in accordance with clinical pathways and medical efficacy. This POJK is effective 3 (three) months after promulgation.

- POJK 37/2025 concerning the Determination of Status and Supervisory Actions of Insurance Companies, Guarantee Companies and Pension Funds, as an amendment to POJK 9/2021 that previously regulated non-bank financial services institutions. The amendment includes guarantee institutions in the regulatory scope of this POJK, given the planned implementation of risk-based supervision in the guarantee industry, while expanding and adjusting the quantitative parameters to determine supervisory status for guarantee institutions and pension funds, as well as expanding OJK's authority to adjust supervisory status during the merger and acquisition process and during the process of increasing paid-up capital. This POJK is effective 6 (six) months after promulgation.

- POJK 39/2025 concerning the Procedures for Collecting Administrative Sanctions in the form of Fines in the Financial Services Sector, following implementation of Government Regulation 41/2024 concerning the Work Plan and Budget of the Indonesia Financial Services Authority (OJK) and Levies in the Financial Services Sector, and POJK 2/2025 concerning Levy Procedures in the Financial Services Sector and Other Revenues.

- POJK 40/2025 concerning the Use of Funds from Public Offerings, issued to increase investor protection, enhance reporting quality and governance in the use of funds from public offerings, as well as ensure the funds from public offerings are realised in accordance with the fund utilisation plan contained within the prospectus.

- POJK 41/2025 concerning the Representative Offices of Financing Institutions, Venture Capital Firms, and Other Financial Services Institutions Headquartered Overseas, which regulates the licensing of opening representative offices, the activities of representative offices, the supervision of representative offices, and the closure of representative offices.

- POJK 42/2025 concerning PVML Financial Reporting Integrity, which regulates financial reporting integrity to ensure correct, accurate, and transparent financial information in the Financial Report. In addition, the POJK regulates the duties and responsibilities of the Board of Directors, the Board of Commissioners, and the Audit Committee, as well as the roles of Controlling Shareholders and Affiliated Parties in the financial reporting process.

- Circular Letter (SEOJK) 29/SEOJK.03/2025 concerning Conventional Commercial Bank Report Publication and Transparency, as the implementation guidelines of POJK 18/2025 concerning Bank Report Transparency and Publication. This OJK circular letter supersedes SEOJK Number 9/SEOJK.03/2020 concerning Conventional Commercial Bank Report Publication and Transparency. It regulates aspects of disclosure of prudential principles, including the disclosure of risk-weighted assets (RWA) and remuneration governance, adjustments to the reporting format, the preparation of technical guidance, as well as harmonisation with the latest prudential principles and international standards, specifically Pillar 3 disclosure practices and regulations concerning related parties in accordance with the Basel Core Principles, to increase transparency and accountability in the conventional commercial banking industry.

- SEOJK 31/SEOJK.03/2025 concerning Commercial Bank Reporting through the OJK Reporting System, which aims to increase the effectiveness and efficiency of bank report submission by streamlining (simplifying) the reports as well as through the digitalisation of reporting to enhance technology-based supervision in OJK. This OJK circular letter implements POJK 22/2025, which regulates the types and formats of reports, as well as the preparation guidelines for periodic and incidental reports. This OJK circular letter also stipulates the timeline for the commencement of online reporting through the APOLO system, providing a transition period for banks.

- SEOJK 34/SEOJK.07/2025 the Business Plan of Digital Financial Asset Traders, which serves as guidelines for Digital Financial Asset Traders when preparing a mature, realistic and comprehensive business plan that describes the development plan and business activities of digital financial asset traders for a period of 1 (one) year, while still adhering to risk management and prudential principles.

- SEOJK 35/SEOJK.06/2025 concerning the Soundness Assessment of Pawnbrokers and Islamic Pawnbrokers, in accordance with the mandate of Article 196, Paragraph (3) and Article 203, Paragraph (8) of POJK 39/2024 concerning Pawnbroking, which regulates assessing the soundness of individual companies, updating the soundness assessment, action plans, reporting, as well as verification and validation by OJK.

- PADK 37/PADK.08/2025 concerning the Delivery of Marketing Information for Financial Products and Services, as comprehensive and standardised guidelines for financial services providers (FSPs) concerning the provision of information, delivery of marketing information, as well as the presentation of product and/or service information in accordance with prevailing laws and regulations.

- PADK 38/PADK.06/2025 concerning the Soundness Assessment of FinTech Peer-to-Peer Lending, in accordance with the mandate of Article 167, Paragraph (3) Article 171, Paragraph (3), and Article 177, Paragraph (8) of POJK 40/2024 concerning FinTech Peer-to-Peer Lending, which regulates assessing the soundness of individual companies, updating the soundness assessment, action plans, reporting, as well as verification and validation by OJK.

- PADK 39/PADK.05/2025 concerning Guarantee Business Units at Conventional General Insurance Companies and Islamic General Insurance Companies, in accordance with the mandate of Article 6, Paragraph (4) of POJK Number 69/POJK.05/2016 concerning Insurance Companies, Islamic Insurance Companies, Reinsurance Companies, and Islamic Reinsurance Companies, as amended by POJK 36/2024. This BOC Member Regulation regulates the institutional requirements for establishing a guarantee business unit, the application of prudential principles, and adequate risk management for general insurance companies and Islamic general insurance companies to expand the scope of their guarantee business based on government assignment. This BOC Member Regulation is effective from 8 December 2025.

- PADK 42/PADK.03/2025 concerning Written Orders for the Resolution of Troubled Banks through Mergers, Amalgamations, Acquisitions, Integrations and/or Conversions (P3IK), in accordance with the mandate of Article 14 of POJK 31/2024 concerning Written Orders. This BOC Member Regulation governs the procedures for issuing a Written Order as an instrument for resolving troubled banks. This POJK focuses on technical implementation provisions, including the scope of conversion, considerations for issuing an order, mechanisms and follow-up actions, eligibility assessments, incentives for compliant banks, and reporting and information disclosure obligations.

- PADK 43/PADK.03/2025 concerning the Implementation of Information Technology by Rural Banks and Sharia Rural Banks, as implementation regulations for POJK 34/2025 concerning the Implementation of Information Technology by Rural Banks and Sharia Rural Banks (POJK PTI BPR/BPRS), which regulates the implementation of governance, as well as the policies and procedures for implementing information technology, risk management, cyber security and resilience guidelines, data management and personal data protection, alongside the reporting format for the implementation of information technology.

- PADK 44/PADK.01/2025 concerning the Procedures for Utilising Supporting Professions in the Financial Services Sector, as implementation regulations for POJK 5/2025 concerning Supporting Professions in the Financial Services Sector, which regulates the registration procedures and continuing education (CE) of supporting professions in the financial services sector.

- Whitelist of Licensed Digital Financial Asset Traders and Registered Digital Financial Asset Traders, as an integral part of the efforts to strengthen consumer protection and maintain the integrity of digital financial assets/crypto assets in Indonesia. The whitelist contains the names of entities and applications/platforms licensed and/or registered by OJK as an official reference for the public to ensure the legality of parties facilitating digital financial assets and crypto transactions. OJK also urges the public to transact only in digital financial assets (crypto assets) through licensed and registered digital financial asset traders listed on the whitelist. In addition, OJK reaffirmed that digital financial asset and crypto asset trading activities are subject to and must comply with applicable licensing regulations.

3. Institutional Strengthening

OJK established a Directorate of Digital Banking Supervision, effective in 2026, to provide more focused and consistent supervision amid rapid digital banking transformation.

4. Risk Mitigation in FinTech Lending

OJK launched an insurance support program for the FinTech P2P lending industry, as outlined in the Roadmap for FinTech P2P Lending 2023–2028, to strengthen risk mitigation and ecosystem resilience.

C. Development and Strengthening of the Sharia Financial Services Sector

The Sharia financial sector demonstrated strong performance in 2025. The Indonesia Sharia Stock Index (ISSI) increased by 43.11 percent (ytd), while Sharia mutual fund AUM rose by 65.07 percent (ytd) to IDR83.44 trillion. Sharia financing grew by 7.67 percent (yoy), sharia financing receivables increased by 14.15 percent, while insurance contributions declined by 5.68 percent.

To strengthen the sharia financial services sector, OJK implemented the following measures:

1. Regulatory Strengthening

- SEOJK No. 32/SEOJK.03/2025 concerning Sharia Commercial Bank and Sharia Business Unit Report Publication and Transparency, as implementation regulations for POJK 18/2025 concerning Bank Report Publication and Transparency, and as an amendment to SEOJK Number 10/SEOJK.03/2020 concerning Sharia Commercial Bank and Sharia Business Unit Report Publication and Transparency. This OJK circular letter regulates the scope, format, preparation, announcement and submission of Publication Reports by Sharia Commercial Banks and Sharia Business Units. Improvements to the reporting format and guidelines for preparing publication reports are consistent with the development of Islamic banking products, the latest prudential regulations, and international standards, such as the Liquidity Coverage Ratio and Net Stable Funding Ratio, as well as leverage ratio and investment product regulations for sharia commercial banks and sharia business units.

- Circular Letter (SEOJK) Number 33/SEOJK.03/2025 concerning Sharia Commercial Bank and Sharia Business Unit Reporting through the OJK Reporting System, as implementation regulations for POJK 22/2025 concerning Commercial Bank Reporting through the OJK Reporting System, and as an amendment to SEOJK Number 27/SEOJK.03/2020 concerning Sharia Commercial Bank and Sharia Business Unit Reporting through the Financial Services Authority Reporting System. This OJK circular letter sets out the implementation guidelines for reporting by sharia commercial banks, sharia business units, and representative offices of foreign banks (KPBLN), applicable to both periodic and incidental reports, alongside provisions on data positions, periodisation, and submission deadlines. In addition, this OJK circular letter also regulates when the first periodic reports and incidental reports must be submitted, along with preparation guidelines.

2. Financial Literacy and Inclusion Initiatives

OJK conducted a series of education and literacy programs, including:

- Routine Meeting of the Sharia Financial Literacy and Inclusion Working Group (POKJA LIKS) in the second semester of 2025, on 9 December 2025. The meeting was officially opened by the OJK Chief Executive of Market Conduct Supervision, Education and Consumer Protection (PEPK), and attended by 83 participants, including internal and external members of POKJA LIKS, representatives of sharia financial services providers, and the National Islamic Economy and Finance Committee (KNEKS). The meeting aimed to gather strategic input and insights on the evaluation of Sharia financial literacy and inclusion implementation in 2025, and to formulate recommendations for program development in 2026.

- Focus Group Discussions (FGD) and workshops for Sharia Financial Literacy and Inclusion (LIKS) implementation on 16-17 December 2025 in Banten. The program serves as a strategic platform to evaluate and formulate improvements to the LIKS program's implementation moving forward, while nurturing a spirit of synergy and collaboration among OJK, industry associations, sharia financial services providers, and self-regulatory organisations (SROs) to strengthen sharia financial literacy and inclusion in Indonesia. The LIKS FGD and workshops were attended by 105 representatives from industry associations, shariah financial services providers, and self-regulatory organisations. The program involved self-development workshops and spiritual motivation, alongside a presentation of the LIKS program plan for 2026, including the opportunities and challenges faced, as part of OJK's joint commitment with all stakeholders to expand access to and the utilisation of Islamic financial products and services sustainably.

- Training of Trainers (ToT) for teachers and religious educators (asatidz) at education facilities under the auspices of Nahdlatul Ulama (NU) to support the implementation of the pilot sharia financial literacy teaching module. The program aimed to build the capacity of teaching staff to deliver systematic, applicable Sharia financial literacy material to their students. The ToT program was implemented on 17 December 2025 and attended by 100 teachers from Ma'arif NU. Hosted at the Haji Agus Salim Cikarang religious high school, the event was also attended by leaders from the Nahdlatul Ulama Executive Board (PBNU) and Subject Matter Experts (SME), who were involved directly in the preparation of the sharia financial literacy teaching modules, thereby strengthening the substance of the material as well as ensuring alignment between the policies, curriculum and learning practices in education units.

- Inaugurating the Sharia Financial Inclusion Centre Ecosystem (EPIKS) at the Minhaajurrosyidiin Pesantren (Islamic boarding school) in East Jakarta on 9 December 2025. The EPIKS inauguration was attended by the OJK Chief Executive of Market Conduct Supervision, Education and Consumer Protection (PEPK), head of the OJK Office in Jakarta, representatives from the Ministry of Religious Affairs in the Special Capital Region of Jakarta, Regional Government Officials from the Special Capital Region of Jakarta, directors from Islamic financial services institutions, as well as leaders from Minhaajurrosyidiin Pesantren. The program's scope of activities included shariah financial literacy targeting students and teachers, as well as local MSMEs, with approximately 800 attendees, to increase understanding and awareness of Islamic financial products and services. In addition, access to Islamic finance was expanded, among other measures, by opening savings accounts for students, activating and optimising student cards, establishing branchless banking agents, providing Reverse Vending Machines (RVMs) integrated with financial transactions to support plastic waste management, and establishing the Sharia Investment Gallery.

- Issuing a khutbah (collection of Islamic sermons) for the sharia insurance, guarantee, and pension fund (PPDP) industry in conjunction with industry associations and the Indonesian Mosque Council (DMI). The khutbah was prepared using a communicative, contextual, and straightforward approach to bridge Sharia values with modern financial practices. During the launch ceremony, a Memorandum of Understanding (MoU) was also signed between DMI, the Indonesia Sharia Insurance Association (AASI), and the Financial Institution Pension Fund Association (ADPLK) to unlock financial education and distribution channels for sharia PPDP products by optimising the mosque network throughout Indonesia.

3. Sharia Business Unit (UUS) Spin-Offs

In accordance with POJK No. 11/2023, by end-2025:

- Two UUS completed spin-offs into full-fledged sharia insurance companies;

- Two UUS transferred portfolios; and

- Six UUS remain in the spin-off process.

The statutory deadline for UUS spin-offs is end-2026.

D. Strengthening OJK Governance

OJK continues to reinforce integrity and good governance across the financial services sector through the following initiatives:

- Integrity Assessment and Anti-Corruption Commitment: As part of its commitment to corruption eradication and integrity enhancement, OJK participated in the Integrity Assessment Survey (Survei Penilaian Integritas – SPI) conducted annually by the Corruption Eradication Commission (KPK). In 2025, OJK achieved a score of 80.56, with a “Maintained” predicate, indicating consistently low corruption risk and the continued effectiveness of OJK’s integrity strengthening programs. This score was also above the average for all government ministries and agencies (72.32).

- Strengthening Internal Audit Capability: In 2025, OJK conducted a capability assessment of its internal audit function based on the Internal Audit Capability Model (IACM) developed by the Institute of Internal Auditors Research Foundation (IIARF). The assessment aims to measure and enhance the internal audit function’s ability to support organisational objectives, strengthen governance, and identify opportunities for improvement. OJK’s IACM score has shown a consistent upward trend, increasing from 82.96 percent in 2020 to 94.51 percent in 2025, reflecting progression from Level 4 to Level 5. This achievement demonstrates OJK’s commitment to international best practices, including the early adoption of the Global Internal Audit Standards (GIAS), to enhance management effectiveness and work processes.

- Collaboration with KPK and Integrity Capacity Building: OJK strengthened governance and integrity through collaboration with KPK by increasing the number of employees certified as Integrity Experts (Ahli Pembangun Integritas – API) and Anti-Corruption Counsellors (Penyuluh Anti Korupsi – PAKSI). As of 2025, 58 OJK employees were API-certified, and 52 employees participated in PAKSI training during the year. In addition, OJK received a score of 98 out of 100 from KPK for its Gratification Control Program (PPG), indicating strong performance in preventing gratification-related risks.

- Anti-Fraud Strategy and Risk Control: In 2025, OJK successfully maintained ISO 37001 (Anti-Bribery Management System – ABMS) certification and expanded its implementation scope to cover all work units within OJK, reinforcing institutional resilience against bribery and fraud risks.

- Quality Management System Certification: OJK also successfully maintained its ISO 9001 (Quality Management System) certification following a surveillance audit conducted by an independent external auditor on 17 November 2025. The certification scope covers key governance functions, including internal audit, risk management, quality control, the gratification control program, and the whistleblowing system.

- Governance Outreach and Integrity Culture Development: To further promote integrity and good governance in a sustainable manner, OJK implemented a series of governance outreach initiatives, including the Governance Insight Forum and Student Integrity Camp. From January to 22 December 2025, these programs reached 87,215 participants, comprising OJK employees and external stakeholders.

Additional initiatives included:

- Commemoration of World Anti-Corruption Day (Hakordia 2025) through:

- An anti-corruption seminar held in collaboration with the Ministry of Women’s Empowerment and Child Protection on 8 December 2025, entitled “Women’s Integrity as State Administrators Against Corruption”; and

- A joint World Anti-Corruption Day event with BPJS Kesehatan on 9 December 2025, entitled “Integrity Moment for BPJS Kesehatan.”

- Public lecture at Yogyakarta State University (UNY) on 10 December 2025, entitled “The Younger Generation and Good Governance: Foundations of a Clean and Accountable Financial Services Sector.” Through this initiative, OJK continues to cultivate integrity awareness among younger generations, encouraging them to act as agents of change by rejecting corruption and recognising the risks of illegal financial products and services.

E. Regulatory Enforcement and Investigation Progress in the Financial Services Sector

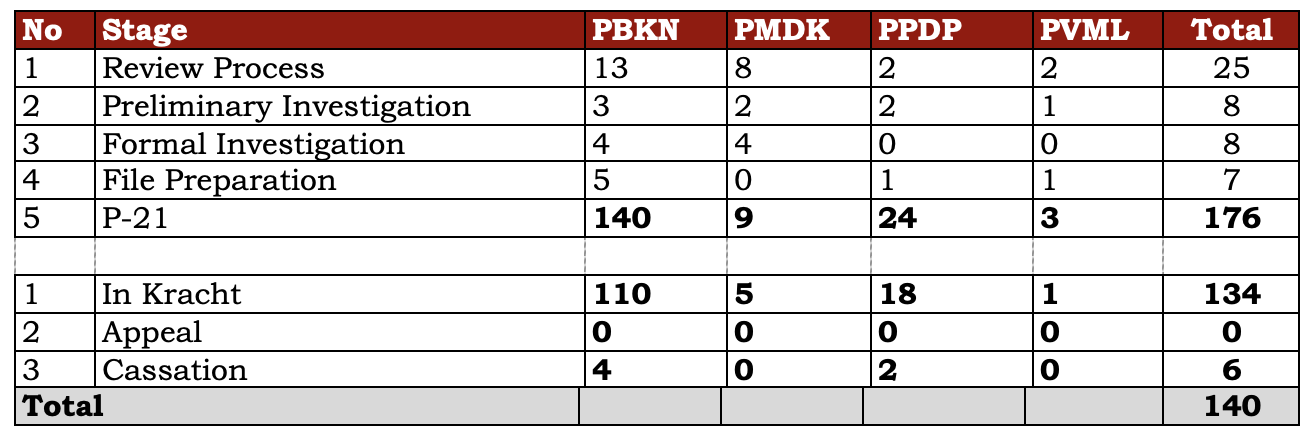

In carrying out its investigative mandate, as of 31 December 2025, OJK investigators had concluded 176 cases, comprising:

- 140 cases in the banking sector;

- nine cases in the capital market, financial derivatives, and carbon exchange (PMDK) sector;

- 24 cases in the Insurance, Guarantee, and Pension Fund (PPDP) industry; and

- three cases involving financing institutions, venture capital firms, microfinance institutions, and other financial service institutions (PVML).

Of these cases, 140 have been resolved through the judicial process, including 134 cases with final and binding decisions (in kracht) and six cases currently at the cassation stage.

OJK investigators continue to coordinate closely with other law enforcement agencies to ensure effective investigation completion and consistent enforcement of financial services sector laws through inter-agency cooperation.

***

Head of the Literacy, Financial Inclusion, and Communication Department – M. Ismail Riyadi

Tel. (021) 29600000; E-mail: humas@ojk.go.id