Policy

Financial Services Sector Stability Maintained Amid Increasing Global Geopolitical Uncertainty (Monthly Board of Commissioners Meeting - June 2025)

Financial Services Sector Stability Maintained Amid Increasing Global Geopolitical Uncertainty

Jakarta, 8 July 2025. The Monthly Board of Commissioners Meeting of the Financial Services Authority (OJK) held on 25 June 2025 assessed that the stability of the Financial Services Sector (SJK) was still maintained despite global economic moderation and escalating geopolitical tensions in the Middle East.

International organisations again downgraded their world economic growth projections for 2025 and 2026. In their latest reports, the World Bank and OECD assessed that the uncertainty surrounding geopolitical developments continues to overshadow the economic recovery outlook moving forward.

Trade uncertainty between the United States (US) and China eased slightly after the framework for a trade agreement between the two countries was reached. Notwithstanding, geopolitical tensions are ramping up again, particularly in the Middle East, in response to the war between Israel and Iran, followed by the US attack on Iran’s three main nuclear facilities. Pressure on financial markets and oil prices also eased after the ceasefire between Israel and Iran came into effect.

Against such an inauspicious backdrop, global economic indicators point to a moderating trend, with most below expectations. This has triggered more accommodative fiscal and monetary policies globally. In the US, despite a downgraded economic growth outlook, the Federal Reserve (the Fed) is yet to lower interest rates, maintaining its benchmark Federal Funds Rate (FFR) in the 4.25-4.50 percent range, awaiting further clarity on tariff policy and its impact on inflation.

At home, the domestic economy remains resilient despite the global turmoil. Inflation continues tracking a downward trend, with core inflation moderating to 2.37 percent (yoy).

Externally, the trade balance in May 2025 amassed a significant surplus following pressures experienced the month earlier. Export performance has improved, primarily driven by positive export growth for agricultural and manufacturing products during the past three months. Such growth effectively offset the declines recorded in exports of mining products and other commodities.

Developments in the Capital Market, Financial Derivatives and Carbon Exchange (PMDK)

Amid turbulent global geopolitical dynamics, the domestic stock market experienced 3.46 percent (mtd) moderation to a level of 6,927.68, or falling 2.15 percent on a year-to-date (ytd) basis. Market capitalisation was recorded at IDR12,178 trillion, down 1.95 percent (mtd) (down 1.28 percent ytd). Meanwhile, non-residents booked a net sell totalling IDR8.38 trillion (mtd) in June 2025 (net sell of IDR53.57 trillion ytd). In general, sectoral index performance (mtd) deteriorated, particularly in terms of the manufacturing industry and financial sector, contrasting stronger performance in the transportation and logistics sector as well as raw materials.

In terms of transaction liquidity, average daily trading value on the domestic stock market (ytd) was recorded at IDR13.29 trillion, up from IDR12.90 trillion in May 2025.

In the bond market, the ICBI bond market index rallied 1.18 percent (mtd) to a level of 414.00, with the average government bond (SBN) yield falling by 8.26 bps (mtm) (down 30.28 bps (ytd). As of 30 June 2025, non-resident investors booked a net sell totalling IDR7.36 trillion (mtd) (ytd: net buy IDR42.27 trillion). In the corporate bond market, non-resident investors recorded a net sell of IDR0.19 trillion (mtd) (ytd: net sell of IDR1.40 trillion).

In the investment management industry, as of 30 June 2025, the value of Assets Under Management (AUM) stood at IDR844.69 trillion (down 0.19 percent mtd or up 0.87 percent ytd), with the Net Asset Value (NAV) of mutual funds recorded at IDR510.15 trillion, down 0.31 percent (mtd) (ytd: up 2.18 percent) and a net subscription of IDR0.45 trillion (mtd) (ytd: net redemption of 2.02 trillion).

Fundraising in the capital market maintained a positive trend, with the value of Public Offerings reaching IDR142.62 trillion, including IDR8.49 trillion of fundraising from 16 new issuers. Meanwhile, 13 Public Offering pipelines remain active, with an indicative estimated value of IDR9.80 trillion.

In terms of fundraising through securities crowdfunding (SCF), since enactment of the SCF regulation until 30 June 2025, a total of 18 providers have been licensed by OJK, with 852 securities issuances from 525 issuers, 182,643 investors, and total SCF funds collected and administered in the Indonesian Central Securities Depository (KSEI) amounting to IDR1.60 trillion.

In the financial derivatives market, from 10 January until 30 June 2025, a total of 97 participants and 19 providers had obtained a principal licence from OJK. Transaction value in the month of June 2025 stood at IDR135.30 trillion, with an average daily transaction value of IDR6.44 trillion (ytd: IDR10.23 trillion per day). The total transaction volume of financial derivatives with securities as underlying assets from 2 January until 30 June 2025 was recorded at 591,381 lots, with an accumulated value of IDR1,309.09 trillion.

Regarding the carbon exchange, from launch on 26 September 2023 until 30 June 2025, there were 112 licensed service users with a total volume of 1,599,322tCO2e and an accumulated value of IDR77.95 billion.

During the period from 20 March to 30 June 2025, 43 issuers planned to perform buybacks without a General Meeting of Shareholders (RUPS), with an estimated buyback fund allocation of IDR22.54 trillion. Of the 43 issuers, 35 have executed buybacks with a realised value of IDR3.38 trillion, accounting for 14.98 percent.

Enforcing PMDK regulations in 2025, OJK has imposed administrative sanctions based on the outcomes of case investigations in the capital market, consisting of administrative sanctions in the form of fines totalling IDR10,780,000,000.00 on 14 entities, the revocation of individual licences on one entity, the revocation of business licences of securities companies on two entities and written warnings on eight entities, as well as the imposition of administrative sanctions in the form of fines totalling IDR17,452,720,000.00 on 251 financial service providers (PUJK) in the capital market and 73 written warnings for late report submissions, along with fines totalling IDR100,000,000.00 and 33 written warnings for other non-case violations, excluding late submissions.

Developments in the Banking Sector (PBKN)

Banking intermediation remained stable with a well-managed risk profile, recording credit growth of 8.43 percent (yoy) in May 2025 (April 2025: 8.88 percent) to reach IDR7,997.63 trillion.

By loan type, investment loans posted the strongest growth at 13.74 percent, followed by consumer loans at 8.82 percent and working capital loans at 4.94 percent (yoy). By bank group, foreign bank branches were the main driver of credit growth in the reporting period, recorded at 11.61 percent (yoy). Based on borrower category, corporate loans posted 11.92 percent growth, while MSME loans grew by 2.17 percent amid consistent efforts in the banking industry to focus on restoring the quality of MSME loans.

Third-party funds (DPK) recorded 4.29 percent (yoy) growth in May 2025 (April 2025: 4.55 percent yoy) to reach IDR9,072 trillion, with demand deposits, savings deposits and time deposits growing by 5.57 percent, 5.39 percent and 2.31 percent (yoy), respectively. Limited time deposit growth, in addition to more attractive demand deposit and savings deposit instruments in terms of yield and flexibility, also stemmed from the increasing diversity of alternative investment instruments available offering higher yields.

Liquidity in the banking industry remained ample in May 2025, with the ratios of liquid assets to non-core deposits (LA/NCD) and liquid assets to third-party funds (LA/TPF) recorded at 110.33 percent (April 2025: 111.32 percent) and 24.98 percent (April 2025: 25.23 percent), respectively, well above the regulatory thresholds of 50 percent and 10 percent. Meanwhile, the liquidity coverage ratio (LCR) was recorded at a level of 192.41 percent.

Credit quality in the banking industry was maintained, as indicated by a gross NPL ratio of 2.29 percent (April 2025: 2.24 percent) and net NPL ratio of 0.85 percent (April 2025: 8.03 percent). Loans at Risk (LaR) remained relatively stable at 9.93 percent (April 2025: 9.92 percent) in line with pre-pandemic levels.

Banking industry resilience also remained solid, as reflected by a high Capital Adequacy Ratio (CAR) of 25.51 percent (April 2025: 25.41 percent), thus providing a robust buffer against risk amid heightened global uncertainty.

The share of Buy Now Pay Later (BNPL) loans disbursed by the banking industry stood at just 0.27 percent of total credit yet continues to record strong annual growth. As of May 2025, the balance of outstanding BNPL loans reported via the Financial Information Services System (SLIK) grew 25.41 percent (yoy) (April 2025: 26.59 percent yoy) to IDR21.89 trillion, with the number of accounts increasing to 24.79 million (April 2025: 24.36 million).

Regarding the serious crackdown on online gambling, which has wide-reaching deleterious impacts on the economy and financial sector, OJK has instructed banks to block approximately 17,026 accounts based on the data submitted by the Ministry of Communication and Digital Affairs. In addition, OJK is following up the reports by also requesting banks to close accounts matching specific Population Identification Numbers (NIK) and mandating Enhanced Due Diligence (EDD).

Developments in the Insurance, Guarantee and Pension Fund Industry (PPDP)

In thePPDP sector, insurance industry assets as of May 2025 stood at IDR1,163.62 trillion, up 3.84 percent (yoy). In the commercial insurance industry, total assets were recorded at IDR939.75 trillion, with growth of 4.30 percent (yoy).

In terms of premium income, commercial insurance industry performance from January-May 2025 stood at IDR138.61 trillion, growing 0.88 percent (yoy), consisting of life insurance premiums that contracted by 1.33 percent (yoy) to IDR72.53 trillion as well as general insurance and reinsurance premiums that grew by 3.43 percent (yoy) to IDR66.08 trillion.

In general, capitalisation of the commercial insurance industry remains solid, with the life insurance as well as general insurance and reinsurance industries, as an aggregate, reporting risk-based capital (RBC) of 480.77 percent and 311.04 percent, respectively (well above the 120 percent threshold).

In terms of non-commercial insurance, comprising the Social Security Agency for Employment (BPJS Ketenagakerjaan) and the Social Security Agency for Health (BPJS Kesehatan), as well as insurance programs for civil servants (ASN), military personnel (TNI) and the police (POLRI) related to occupational accident compensation and accidental death insurance, total assets were recorded at IDR223.87 trillion with growth of 1.95 percent (yoy).

In the pension fund industry, total assets as of May 2025 grew 9.20 percent (yoy) to reach IDR1,572.15 trillion. In terms of voluntary pension programs, total assets recorded growth of 5.05 percent (yoy) with a value of IDR391.33 trillion.

Regarding compulsory pension programs, consisting of old age benefits and pension benefits under the auspices of BPJS Ketenagakerjaan,as well as old-age savings and pension contribution accumulation programs for civil servants (ASN), military personnel (TNI), and the police (POLRI), total assets reached IDR1,180.82 trillion, growing 10.65 percent (yoy).

In terms of guarantee companies, as of May 2025, asset value grew 0.53 percent (yoy) to IDR47.32 trillion.

Concerning regulatory enforcement and consumer protection in the PPDP sector, OJK took the following measures:

- Fulfilling the first stage of the equity enhancement obligations for 2026 in accordance with OJK Regulation (POJK) Number 23 of 2023, based on the monthly reports submitted as of May 2025, a total of 106 out of 144 insurance and reinsurance companies have already met the minimum equity requirements for 2026.

- OJK continues implementing various efforts to resolve ongoing issues plaguing financial service institutions (FSIs) through special surveillance, as applied to six insurance and reinsurance companies as of 24 June 2025, to improve their financial condition in the interest of the policyholders. In addition, nine pension funds have also been placed under special surveillance.

Developments in Financing Institutions, Venture Capital Firms, Microfinance Institutions and Other Financial Service Institutions (PVML Sector)

In the PVML sector, the financing receivables of finance companies (PP) grew 2.83 percent (yoy) in May 2025 (April 2025: 3.67 percent yoy) to IDR504.58 trillion, underpinned by working capital financing that grew by 10.34 percent (yoy).

Finance companies managed their risk profile effectively, as reflected by a gross non-performing financing (NPF) ratio of 2.57 percent (April 2025: 2.43 percent) and net NPF ratio of 0.88 percent (April 2025: 0.82 percent). The gearing ratio of finance companies was recorded at 2.20x (April 2025: 2.23x), which is significantly below the 10x cap.

Venture capital financing in May 2025 grew 0.88 percent (yoy) (April 2025: 1.04 percent yoy), with a value of IDR16.35 trillion (April 2025: IDR16.49 trillion).

In the FinTech peer-to-peer (P2P) lending industry, outstanding financing in May 2025 grew 27.93 percent (yoy) (April 2025: 29.01 percent yoy), with a value of IDR82.59 trillion. The aggregate NPL ratio (TWP90) stood at 3.19 percent in the reporting period (April 2025: 2.93 percent).

According to the Financial Information Services System (SLIK), Buy Now Pay Later (BNPL) financing disbursed by finance companies in May 2025 increased by 54.26 percent (yoy) (April 2025: 47.11 percent yoy) to IDR8.58 trillion, with a gross NPF ratio of 3.74 percent (April 2025: 3.78 percent).

Regarding regulatory enforcement and consumer protection in the PVML sector, OJK took the following measures:

- OJK revoked the business licence of PT Sarana Sulteng Ventura through OJK BoC Decree Number KEP-22/D.06/2025, dated 16 June 2025. The business licence was revoked after the business entity (company) was unable to fulfil the minimum equity requirements prior to the deadline for sanctions, including the suspension of business activities.

- Currently, three out of 145 finance companies have failed to meet the minimum equity requirements of IDR100 billion. In addition, 14 out of 96 P2P lenders have failed to meet the minimum equity requirements of IDR12.5 billion. Of the 14 P2P lenders aforementioned, five have submitted commitment and action plans to fulfil the minimum equity requirements, two sharia P2P lenders have submitted action plans for mergers, and seven other P2P lenders are currently in the process of exploring potential strategic investors. Meeting the minimum equity requirements will further enhance the resilience and competitiveness of P2P lenders and, ultimately, strengthen the industry overall. OJK continues taking the measures necessary based on progress action plans to fulfil the minimum equity requirements in the form of capital injections from shareholders as well as from credible local/foreign strategic investors, while encouraging consolidation, including the return of business licences.

- Enforcing compliance and integrity in the PVML sector, OJK in June 2025 imposed administrative sanctions on 18 finance companies, five venture capital companies, 17 P2P lenders, two private pawnbrokers, one special financial institution and two microfinance institutions for violations of prevailing OJK Regulations (POJK), as well as based on supervisory findings and/or follow-up inspections. The administrative sanctions consisted of 45 fines and 55 written warnings. OJK expects the enforcement measures to foster good governance, prudence and compliance in the PVML sector and, ultimately, improve performance and optimise the industry’s contribution.

Developments in Financial Sector Technology Innovation (ITSK), Digital Financial Assets and Crypto Assets (IAKD Sector)

1.Regulatory sandbox implementation:

- Since promulgation of OJK Regulation (POJK) Number 3 of 2024 concerning the Implementation of Financial Sector Technology Innovation (ITSK), interest from ITSK providers to become OJK sandbox participants has been overwhelming. As of June 2025, OJK received 205 consultation requests from prospective sandbox participants. Of that total, 119 parties have submitted consultation forms and 113 have conducted consultations.

- OJK has received 18 applications for sandbox participants, eight of which were approved, consisting of seven ITSK providers with Digital Financial Asset and Crypto Asset (AKD-AK) business models and one ITSK provider from the Market Support category. Four applications to become sandbox participants are currently under review, consisting of three providers for the AKD-AK business model and one provider with an open finance business model.

2. ITSK Provider Registration:

As of June 2025, a total of 47 ITSK providers have submitted registration applications to OJK, 30 of which have been designated as registered ITSK providers, consisting of 10 Innovative Credit Scoring (ICS) providers and 20 Financial Service Aggregators (PAJK). The designation of registered status for the 30 ITSK providers denotes the completion of the registration process for allITSK providers with the ICS and PAJK business models, which have completed the OJK sandbox process. In accordance with the implementation of OJK Regulation (POJK) Number 29 of 2024 concerning Innovative Credit Scoring (ICS) and OJK Regulation (POJK) Number 4 of 2025 concerning Financial Service Aggregators (PAJK), prospective ICS andPAJK service providers can now apply to OJK for a licence. This change reflects OJK's commitment to enhancing licensing efficiency, while helping to accelerate technological innovation in the financial services sector.

3. Based on the reports submitted as of May 2025, ITSK providers registered with OJK have successfully established 987 partnerships with financial service institutions (FSIs) across various sectors, including the banking industry, finance companies, insurance, securities companies, online lenders, microfinance institutions and pawnbrokers, as well as with information technology service providers and data source providers.

4. During the month of May 2025, Financial Service Aggregators (PAJK) successfully facilitated partner-approved transactions worth IDR2.1 trillion, with a total of 928,396PAJK users distributed throughout the Indonesian archipelago. In addition, the number of credit score data requests received byInnovative Credit Scoring (ICS) providers amounted to 26.37 million total hits in the reporting period. Such developments indicate that the services offered by ITSK providers have contributed to boost activity and accelerate market deepening in the financial services sector, while increasing accessibility and inclusion in the use of financial products and services.

5. As of June 2025, a total of 1,153 tradeable crypto assets were recorded. OJK has approved licences for 23 entities within the crypto trading ecosystem,consisting of one crypto exchange, one clearing and settlement institution, one custodian, and 20 crypto asset traders. Meanwhile, OJK is currently processing the licenses for another 10 prospective crypto asset traders.

6. Concerning the development of crypto asset activities in Indonesia, the number of consumers continues tracking an upward trend, reaching 14.78 million consumers in May 2025 (April 2025: 14.16 million consumers). The value of crypto asset transactions in May 2025 was recorded at IDR49.57 trillion (April 2025: IDR35.61 trillion), indicating maintained consumer confidence and robust market conditions.

7. Strengthening the IAKD ecosystem, OJK on 25 June 2025 approved the Indonesia Blockchain Association (ABI) as the respective association forITSK providers. Currently, therefore, there are 3 (three) official associations for ITSK providers in the IAKD sector, namely the Indonesia FinTech Association (Aftech), Indonesia Sharia FinTech Association (AFSI), and the Indonesia Blockchain Association (ABI). The presence of such associations in the IAKD sector is expected to serve as strategic partners of OJK in terms of nurturing accountable technological innovation in the financial system (ITSK) that prioritises compliance, consumer protection and increasing digital financial literacy in the community.

8. SupportingIAKD sector development, OJK has received approval from the Ministry of Finance to adjust the levy payment obligations for service providers licensed by OJK in the IAKD sector. The adjustments take into consideration OJK's ongoing efforts to develop theIAKD industry nationally, as well as the general state of the IAKD industry, which is currently at the nascent stage of operational activity. Consequently,ITSK providers in the IAKD sector will be subject to a 0% levy rate in 2025, followed by incremental increases in subsequent years.

Developments in Market Conduct Supervision, Education and Consumer Protection (PEPK)

From 1 January to 30 June 2025, OJK hosted 2,937 financial education activities that reached more than 6,170,698 participants throughout Indonesia. The Sikapi Uangmu digital platform, which serves as a dedicated communication channel for financial education content to the public through a minisite and application, published 170 pieces of educational content, reaching a total of 1,098,989 viewers. In addition, 19,948 users accessed the Financial Education Learning Management System (LMSKU), with modules accessed a total of 5,950 times and 2,662 module completion certificates issued.

The various efforts taken to increase financial literacy were further supported by strengthening the financial inclusion program in collaboration with the Regional Financial Access Acceleration Teams (TPAKD) in all 38 provinces and 514 regencies/cities in Indonesia.

OJK implemented the following financial literacy and inclusion initiatives in June 2025:

- From January to 30 June 2025, OJK implemented the GENCARKAN flagship program through more than 22,000 initiatives that engaged 110.3 million participants. Such activities included more than 11,000 offline financial education activities that reached 4.8 million participants, coupled with more than 10,000 pieces of digital financial education content that reached 105.4 million viewers.

- Discussion activities and Training of Trainers (ToT), entitled “OJK Enables Indonesian Financial Literacy Ambassadors (OJK PEDULI) in the Mass Media” on 16 June 2025 in Jakarta. The activities aimed to enable mass media editors and journalists to become Financial Literacy Ambassadors, thereby increasing public understanding when using financial products and services as well as avoiding fraudulent and illegal financial practices. Based on OJK data for the period from April-June 2025, a total of 6,460 Financial Literacy Ambassadors were registered in the OJK PEDULI system.

- As a form of appreciation for the banking industry, education units and regional governments that have actively participated and contributed to supporting the implementation of the One Account, One Student (KEJAR) program, OJK will present the KEJAR Awards 2025 as the culmination of Indonesia Savings Day. Supporting the activities, OJK socialised the KEJAR Awards to representatives of all commercial banks, Islamic banks, regional government banks, and (sharia) rural banks on 5 June 2025. The KEJAR Awards 2025 will involve the participation of 503 banks and 412,449 educational units spanning Indonesia.

- Strengthening and optimising the Regional Financial Access Acceleration Teams (TPAKD), OJK has implemented:

- Socialisation activities in synergy with relevant government ministries/agencies to support the implementation and integration of the Regional Financial Access Index (IKAD) into the Medium-Term Regional Development Plan (RPJMD) 2025-2030, the Strategic Plan (Renstra) and the Regional Government Performance Plan (RKPD). In addition to the socialisation activities held on 9 May 2025, which were attended by all leaders of Bappeda and TPAKD throughout Indonesia, OJK also hosted follow-up socialisation activities in the former Pekalongan Residency area at the TPAKD Plenary Meeting on 18 June 2025, socialisation activities in Maluku province at the TPAKD Plenary and Rakorda Meetings on 28 May 2025, and socialisation activities in Bandung Regency on 20 May 2025.

- TPAKD coaching clinics in Banten Province on 4 June 2025 and the Jakarta Special Capital Region on 23 June 2025 to provide technical coaching and practical understanding to TPAKD team members towards optimising the role and function of TPAKD teams in each region and improving the effective formulation of work programs, setting and achieving targets, implementing activities as well as structured and sustainable reporting through the TPAKD information system.

In terms of consumer services, from 1 January to 13 June 2025, OJK received 222,679 service requests through the Consumer Protection Portal Application (APPK), including 20,115 complaints. Of the total complaints, 7,457 originated from the banking sector, 7,697 from the FinTech industry, 4,046 from finance companies, and 648 from insurance companies, with the remainder relating to the capital market and other non-bank financial industries.

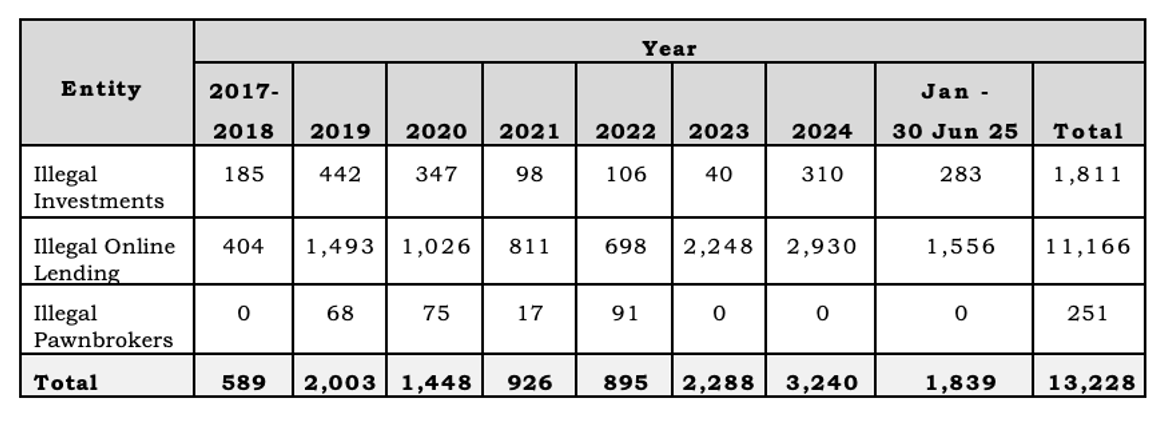

Seeking to eradicate illegal financial activities, from 1 January to 30 June 2025, OJK received 8,752 complaints relating to illegal entities. Of that total, 7,096 complaints were received in relation to illegal online loans along with 1,656 complaints concerning illegal investment activity.

The number of illegal entities shut down/blocked is recapitulated as follows:

Enforcing consumer protection regulations through the Task Force for the Eradication of Illegal Financial Activities (Satgas PASTI), during the period from 1 January to 30 June 2025, OJK:

- identified and shut down 1,556 illegal online lending entities and 283 illegal investment offers on various websites and applications with the potential to harm the public.

- Satgas PASTI acquired the contact numbers of debt collectors from illegal online lending entities and submitted a request to the Ministry of Communication and Digital Affairs of the Republic of Indonesia to block 2,422 contact numbers. In addition, Satgas PASTI also monitored scam reports through the Indonesia Anti-Scam Centre (IASC) and found 22,993 contact numbers reported by scam victims. As a follow-up action,Satgas PASTI coordinated with the Ministry of Communication and Digital Affairs of the Republic of Indonesia to block the contact numbers reported.

Since its launch on 22 November 2024 to 30 June 2025, IASC received 166,258 reports, consisting of 108,037 reports submitted by victims through financial sector entities (banks and payment system operators), which were subsequently inputted into theIASC system, along with 58,221 reports submitted by victims directly into the IASC system. In total, 267,962 accounts were reported and 56,986 accounts were blocked. To date, total reported financial losses amount to 3.4 trillion, with 558.7 billion of victim funds blocked. IASC will continue to enhance its capacity to expedite fraud and scam case handling in the financial sector.

Enforcing consumer protection regulations, OJK issued written warnings and/or administrative sanctions during the period from 1 January to 30 June 2025 in the form of 85 Written Warnings to 72 Financial Service Providers (FSP), 13 Written Instructions to 13 FSPs and 23 Fines to 22 FSPs. In addition, during the period from 1 January to 22 June 2025, a total of 122 FSPs were required to compensate consumer losses amounting to IDR26.23 billion and USD3,281.

In terms of overseeing market conduct, OJK has enforced regulations through Administrative Sanctions based on the results of onsite/offsite supervision. From 1 January to 30 June 2025, OJK issued two Administrative Sanctions in the form of Written Warnings and two Administrative Sanctions in the form of Fines for violations of consumer protection regulations relating to the information provided in advertisements. Seeking to prevent a recurrence of similar violations, OJK also issued orders for specific corrective actions, including the removal of advertisements that do not comply with prevailing provisions.

OJK Policy Direction

Maintaining the stability of the financial services sector and expanding the sector's role in supporting national economic growth, OJK implemented the following policy measures:

A. Policies to Maintain Financial System Stability

OJK monitors and conducts regular assessments of global geopolitical conditions and developments with the potential to amplify financial market volatility and impact the performance of real sector debtors exposed to the associated risks. In addition, OJK also requires financial service institutions (FSIs) to evaluate the latest developments and conduct follow-up assessments to enable and ensure timely and appropriate mitigation actions.

B. Policies for Developing and Strengthening the Financial Services Sector and Market Infrastructure

1.OJK has finalised or issued:

- Circular Letter (SEOJK) Number 8/SEOJK.03/2025 concerning Implementation of the Compliance Function for Rural Banks and Sharia Rural Banks as implementation guidelines for OJK Regulation (POJK) Number 9 of 2024 concerning the Implementation of Governance for Rural Banks and Sharia Rural Banks. The SEOJK regulates, among others, general policies for fostering a compliance culture and implementing compliance functions, independence requirements as well as the duties and responsibilities of the Board of Directors and Compliance Unit or Executive Officers responsible for the compliance and reporting functions, and formats.

- Circular Letter (SEOJK) Number 9/SEOJK.03/2025 concerning Implementation of the Internal Audit Function for Rural Banks and Sharia Rural Banks as implementation guidelines for OJK Regulation (POJK) Number 9 of 2024 concerning the Implementation of Governance for Rural Banks and Sharia Rural Banks. The SEOJK regulates, among others, general policies for internal audits, the organisational structure of internal audits, the implementation of internal audits and reporting on the implementation of the internal audit function. The SEOJK provides a reference for the minimum standards when compiling internal guidelines for the internal audit function at rural banks and Sharia rural banks, which is expected to foster the implementation of an effective and efficient internal audit function.

- Circular Letter (SEOJK) Number 14/SEOJK.03/2025 concerning the Implementation of Governance for Commercial Banks following the promulgation of OJK Regulation (POJK) Number 17 of 2023 concerning the Implementation of Governance for Commercial Banks. The SEOJK regulates 16 pillars/factors to assess governance implementation, the scope and submission procedure of the governance implementation report, as well as a self-assessment matrix regarding governance implementation.

- On 30 June 2025, OJK issued SEOJK Number 15/SEOJK.03/2025 concerning the Implementation of Governance for Sharia Rural Banks, as the implementation guidelines for OJK Regulation (POJK) Number 9 of 2024 concerning the Implementation of Governance for Rural Banks and Sharia Rural Banks, and POJK Number 24 of 2024 concerning the Implementation of Sharia Governance for Sharia Rural Banks. The SEOJK serves as implementation guidelines concerning 13 aspects of sharia rural bank governance, the format and scope for self-assessments of sharia rural bank governance implementation, as well as the types of reports associated with the implementation of governance at sharia rural banks. Promulgation of the SEOJK is expected to help strengthen the comprehensive implementation of governance for sharia rural banks.

- Circular Letter (SEOJK) Number 10/SEOJK.04/2025 concerning the Electronic Submission of Ownership Reports or Changes in Ownership of Public Company Shares and Reports on Pledging Activities at Public Companies, following promulgation of OJK Regulation (POJK) Number 4 of 2024 concerning the Submission of Ownership Reports or Changes in Ownership of Public Company Shares and Reports on Pledging Activities at Public Companies. The SEOJK regulates, among others, the electronic submission of ownership reports or changes in ownership of public company shares and reports on pledging activities at public companies, the providers of electronic reporting systems and publication systems, as well as the electronic submission of reports in cases of force majeure.

- Circular Letter (SEOJK) Number 11/SEOJK.05/2025 concerning the Periodic Reports of Pension Funds, following the issuance of OJK Regulation (POJK) Number 21 of 2024 concerning the Periodic Reports of Pension Funds. The SEOJK regulates, among others, the format, structure and submission procedures for periodic reports in the pension fund industry.

- Circular Letter (SEOJK) Number 12/SEOJK.05/2025 concerning Work Competency Certification for Insurance Companies, Guarantee Institutions, Pension Funds and Special Institutions in the Insurance, Guarantee and Pension Fund Sectors, following the issuance of OJK Regulation (POJK) Number 34 of 2024 concerning the Development of Human Resource Quality for Insurance Companies, Guarantee Institutions, Pension Funds and Special Institutions in the Insurance, Guarantee and Pension Fund Industry. The SEOJK regulates, among others, occupational competency certification and other competency certification in the Insurance, Guarantee and Pension Fund (PPDP) Industry as well as Special Institutions in the IGPF industry.

- Circular Letter (SEOJK) Number 13/SEOJK.05/2025 concerning the Periodic Reports of Insurance Brokers, Reinsurance Brokers and Loss Assessors, following issuance of OJK Regulation (POJK) Number 22 of 2024 concerning the Periodic Reports of Insurance Companies. The SEOJK regulates, among others, the format, structure and submission procedures for periodic reports, submitting corrections to periodic reports and the deferral of the deadline for submitting the periodic reports and/or corrections to the periodic reports of insurance companies.

2. OJK has finalised drafting:

- Draft OJK Regulation (RPOJK) concerning Fit and Proper Tests and the Reassessment of Main Parties in the Financial Sector Technology Innovation, Digital Financial Assets and Crypto Assets (IAKD) Sector, which regulates the factors, procedures and designations of the results of Fit and Proper Tests, the reassessment procedures for main parties (PKPU), as well as the final results and consequences of the PKPU.

- Draft Circular Letter (RSEOJK) concerning Anti-Money Laundering/Combating the Financing of Terrorism and Proliferation Financing (AML/CFT/CPF) for Digital Financial Asset Traders, as implementation guidelines for OJK Regulation (POJK) Number 8 of 2023 concerning the Implementation of AML/CFT/CPF in the Financial Services Sector. The RSEOJK regulates a risk-based approach to AML/CFT/CPF program implementation, active supervision of the board of directors and board of commissioners, policies and procedures, internal controls, management information systems, human resources (HR), as well as reporting for Digital Financial Asset Traders.

3. OJK is drafting:

- Draft POJK concerning the Implementation of Integrated Governance for Financial Conglomerate Holding Companies (PIKK) following the issuance of POJK Number 30 of 2024 concerning Financial Conglomerates and Financial Conglomerate Holding Companies. The draft POJK amends POJK Number 18/POJK.04/2014 concerning Governance for Financial Conglomerates and regulates more equitable governance for Operational and Non-operational PIKK.

- Draft POJK concerning the Implementation of Investment Manager (IM) Business Activities. The draft POJK revises Bapepam Regulation Number V.A.3 concerning the Licensing of Securities Companies Operating as Investment Managers. Among others, the draft POJK regulates licensing requirements, business activity classifications, reporting and the revocation of business licences.

- Draft POJK concerning the Implementation of Securities Companies Operating as Securities Underwriters and Securities Broker-Dealers, which will supersede OJK Regulation (POJK) Number 20/POJK.04/2016. The draft POJK regulates, among others, the categorisation of securities company business activities, the requirements that must be fulfilled by securities companies based on business activity, licensing application procedures for underwriters and broker-dealers, sharia-compliant business activities, single presence policy, business license revocation and obligations.

- Draft SEOJK concerning Insurance Premium Rates for Property and Motor Vehicles as an amendment to current insurance premium regulations. The draft SEOJK regulates insurance premium rates for battery electric vehicles (BEV) and adjusts several rates for property occupation.

- Draft SEOJK concerning Guarantee Business Units (UUP), as mandated by OJK Regulation (POJK) Number 36 of 2024 for insurance companies performing guarantee activities based on government assignments. The draft SEOJK, among others, regulates the criteria and scope of establishing a Guarantee Business Unit (UUP) up to 6 months since enactment of POJK Number 36 of 2024 (up to December 2025).

- Draft SEOJK concerning Good Governance Implementation Reports for Financing Institutions, Venture Capital Firms, Microfinance Institutions and Other Financial Service Institutions (PVML), as implementation guidelines of OJK Regulation (POJK) Number 48 of 2024 concerning Good Governance for PVML, which regulates transparency in the implementation of good governance, self-assessment guidelines and submission procedures for good governance implementation reports, among others.

4. OJK will draft an OJK Regulation (POJK) concerning Strengthening the Health Insurance Ecosystem following a Work Meeting between Commission XI of the House of Representatives of the Republic of Indonesia (DPR-RI) and OJK. Consequently, the provisions contained within Circular Letter (SEOJK) Number 7 of 2025 concerning the Implementation of Health Insurance Products (SEOJK Number 7 of 2025), originally scheduled for promulgation on 1 January 2026, have been deferred and will be regulated in the upcoming POJK.

5. Following issuance of OJK Regulation (POJK) Number 30 of 2024 concerning Financial Conglomerates and Financial Conglomerate Holding Companies (PIKK), OJK is currently processing licences to establish the institutional arrangements for Financial Conglomerate Holding Companies (PIKK).

6. OJK has conducted socialisation activities on reporting the implementation of Anti-Fraud Strategies (SAF) in accordance with OJK Regulation (POJK) Number 12 2024 concerning the Implementation of Anti-Fraud Strategies for Financial Service Institutions (FSIs), targeting commercial banks as well as rural banks and sharia rural banks with minimum core capital of IDR50 billion. The socialisation activities serve as preparation for submitting SAF implementation reports in the first semester of 2025, to be submitted no later than 31 July 2025, as well as early preparation for the second stage of reporting by FSIs planned for 31 January 2026. The socialisation activities focused on procedures for completing and reporting SAF implementation in order to mitigate the technical constraints that emerged during the first phase of reporting implemented in January 2025 and to increase bank understanding to ensure accurate and timely report completion considering that the SAF report will be available via the SIPELAKU application.

7. OJK hosted a Coordination Meeting for the Financial System Stability Committee (KSSK) on 24 June 2025, attended by leaders/officials from the Ministry of Health, National Population and Family Planning Agency (BKKBN), National Agency of Drug and Food Control (BPOM) and Social Security Agency for Health (BPJS Kesehatan). The meeting aimed to strengthen synergy and coordination among stakeholders when formulating strategic policies for the health sector, which includes strengthening a sustainable health financing system and enhancing the quality of public health services.

8. OJK launched the Agent Database and Insurance Policy Database on 30 June 2025 as an integral part of the efforts to strengthen data infrastructure and governance in the national insurance industry, while enhancing the legality and professionalism of insurance agents through an integrated digital registration system via the SPRINT application, which is connected to the applicable associations and digital identity in the form of a QR code. The Insurance Policy Database is part of the mandatory monthly reporting of policy data through the APOLO system, commencing in June 2025, to support risk-based supervision (RBS), prepare for the implementation of the policy underwriting program in 2028 as well as strengthen data accuracy and transparency across the industry.

9. Strengthening risk management in the online lending industry, OJK has:

- required the industry to apply more stringent repayment capacity principles and electronic Know Your Customer (e-KYC) as the basis for disbursing funding,

- stipulated that commencing 31 July 2025, online lenders must participate as reporting entities in the Financial Information Services System (SLIK) in accordance with OJK Regulation (POJK) Number 11 of 2024, as the second amendment to POJK Number 18/POJK.03/2017 concerning Reporting and Requesting Debtor Information through the Financial Information Services System (SLIK).

10. Increasing digital financial literacy in the community and developing innovative solutions to create a more secure, transparent and trusted digital financial ecosystem, OJK hosted several activities as follows:

- On 28 May 2025, OJK hosted a Digital Financial Literacy (DFL) event atUniversitas Pendidikan Muhammadiyah Sorong in West Papua, which aimed to increase public understanding of digital financial products and services, including crypto assets, as well as the associated risks and benefits.

- On 5 June 2025, OJK in synergy with Bank Indonesia hosted the kick-off ceremony for theOJK-BI Hackathon 2025, running from June until September 2025, entitled Empowering the Future: Innovating Digital Services and Financial Solutions for Inclusive Growth and a Resilient Economy. At the event, OJK promoted the main theme of Risk Management and Consumer Protection as well as the subthemes of Smart Contract Audits and On-chain Analysis. OJK-BI Hackathon 2025 is open to the public in two categories, namely professionals and students.

11. In relation to the draft POJK concerning MSME Access to Finance in consultation with the House of Representatives (DPR), OJK hosted socialisation activities for government ministries and agencies, Bank Indonesia, as well as leaders of financial service institutions (FSIs) and industry associations, which is expected to strengthen the direction of structured MSME development policy in terms of quantity and quality by requiring banks and non-bank financial institutions (NBFIs) to offer inclusive, efficient and affordable financing schemes for micro, small and medium enterprises (MSMEs).

12. Regarding the handling of online gambling and other financial crimes, banks were urged to intensify their handling efforts for online gambling and other financial crimes, which includes tighter monitoring of dormant accounts to avoid their illicit use for financial crime, while enhancing banking industry effectiveness in terms of controlling account buying and selling, submitting Suspicious Financial Transactions Reports (LTKM) to the Indonesian Financial Transaction Reports and Analysis Centre (INTRAC) concerning the use of accounts by suspected criminals, analysing flows of funds and implementing cyber patrols to combat the misuse of bank accounts and logos in cyberspace.

13. Responding to the growing risk of cyber incidents that pose a threat to the stability of the financial sector, OJK has strengthened information technology regulations in the banking sector and will establish a task force for handling cyber incidents to ensure a more coordinated, rapid and effective response. OJK also urges all financial services industry players to strengthen cyber resilience and increase coordination with regulators to maintain national financial system security and integrity.

C. Development and Strengthening of Sharia Financial Services Sector

In the sharia financial industry, the Indonesia Sharia Stock Index (ISSI) rallied 5.19 percent (ytd), while the Assets Under Management (AUM) of sharia mutual funds posted 10.45 percent (ytd) growth to reach IDR55.83 trillion. Meanwhile, sharia banking intermediation maintained positive annual growth (yoy), with Islamic finance growing 9.18 percent, sharia insurance contributions growing 0.23 percent and sharia financing receivables growing 9.12 percent. Following Article 9 of OJK Regulation (POJK) Number 11 of 2023, 41 companies have submitted Sharia Unit Spin-Off Plans (RKPUS), of which 29 companies have declared their intention to spin off a sharia unit by establishing a new company, with the remaining 12 planning to transfer their portfolios to other existing companies. In 2025, 18 companies are planning to spin off their sharia unit by establishing a new company and eight companies will transfer their portfolios to other companies. Since May 2025, one sharia business unit (Islamic window) has begun the spin-off process by establishing a new company.

OJK also continued strengthening strategic alliances and collaboration in the development of Islamic finance, which includes increasing Islamic financial literacy and inclusion as follows:

- Drafting RSEOJK concerning Governance for Sharia Rural Banks as implementation guidelines for OJK Regulation (POJK) Number 9 of 2024 concerning the Implementation of Governance for Rural Banks and Sharia Rural Banks and POJK Number 24 of 2024 concerning Asset Quality at Sharia Rural Banks. The draft SEOJK will regulate implementation guidelines for 13 aspects of governance atSharia Rural Banks, the format and scope of self-assessments regarding governance implementation at Sharia Rural Banks, as well as the types of reports associated with governance implementation at Sharia Rural Banks.

- OJK collaborated with the National Islamic Economy and Finance Committee (KNEKS) to host the School of Sharia (SOS) event on 19 June 2025 through the Training of Trainers (ToT) for all religious instructors and the Islamic Financial Inclusion Centre Pre-Ecosystem (Pra-EPIKS), targeting village-owned enterprises (BUMDes) in Lampung Province. Pra-EPIKS activities will be followed by efforts to unlock access to Islamic finance for BUMDes to facilitate sharia-compliant financial services in village communities. The activities were also in line with theDesaku Maju program initiated by the Lampung Provincial Government to optimise village economic potential and development through BUMDes institutions.

- OJK continued increasing Islamic financial literacy and inclusion through strategic alliances, including through the Islamic Financial Literacy and Inclusion Working Group (POKJA LIKS), created to provide recommendations/inputs for the Islamic financial literacy and inclusion development strategy. OJK hosted the POKJA LIKS Meeting in the first semester of 2025 on 30 June 2025, which was attended by all POKJA LIKS members, including OJK and external parties, namely representatives from the National Sharia Board of the Indonesian Council of Ulama (DSN-MUI), industry associations, self-regulatory organisations (SRO), Islamic Economic Society (MES), Indonesian Association of Islamic Economists (IAEI) as well as prominent figures in the effort to increase Islamic financial literacy. The meeting was also attended by the OJK Chief Executive of Market Conduct Supervision, Education and Consumer Protection (PEPK), as board member, expressing her expectation that POKJA LIKS will develop innovative Islamic financial education strategies, while expanding public access to the benefits of Islamic finance. Furthermore, OJK also presented the results of the National Financial Literacy and Inclusion Survey (SNLIK) 2025, the current challenges facing Islamic financial inclusion and plans for future Islamic financial literacy and inclusion programs.

- Following the collaborative implementation of the Sahabat Ibu Cakap Islamic Financial Literacy Program (SICANTIKS) between OJK and PT Permodalan Nasional Madani (PNM), which began in Palembang on 17 May 2025, a series of educational webinars will be held to engage associates of the MSME Prosperous Family Economy Program (Mekaar) throughout Indonesia. Batch II of the SICANTIKS educational webinars were presented online on 21 June 2025, attracting 4,964 participants in Jakarta, Depok, Bekasi, Bogor, Serang, Tangerang and Bengkulu. OJK took the opportunity to deliver educational materials introducing Islamic finance, while creating awareness of illegal financial activities and financial management. OJK also conducted socialisation activities concerning the OJK PEDULI Financial Literacy Ambassadors to nurture Training of Community (ToC) activities for Mekaar associates, including weekly group meetings in local communities.

D. Strengthening OJK Governance

1.Strengthening integrity and good governance in the financial services sector, OJK received an unqualified opinion (WTP) from the Audit Board of the Republic of Indonesia for the OJK Financial Statements 2024. OJK remains firmly committed to strengthening governance, integrity and accountability consistently and sustainably.

2. As an integral part of strengthening internal governance, OJK kicked off preparations for the implementation of Internal Control Over Financial Reporting (ICoFR) in OJK to ensure effective and optimal ICoFR implementation in OJK through all stages prior to full implementation at the end of 2025.

3. OJK constantly improves collaboration with all stakeholders to strengthen governance and integrity in the financial services sector sustainably, which included:

- The Integrity Assessment Survey (SPI) 2025 discussion forum in synergy with the Corruption Eradication Commission (KPK), BPS-Statistics Indonesia and the Social Security Agency for Health (BPJS Ketsehatan) on 3 June 2025 to discuss improving the sustainable implementation of best practices to establish a culture of integrity following the outcomes of SPI 2024.

- Student Integrity Campaign (In Camp) at Universitas Lambung Mangkurat on 16 June 2025, attended by more than 800 academics to instil the values of integrity among the younger generation through an inclusive approach.

- Governance Insight Forum, entitled Building a Financial Services Sector with Integrity with OJK in Banjarmasin on 17 June 2025, attended by speakers and resource persons from the Corruption Eradication Commission (KPK), Audit Board of the Republic of Indonesia (BPK), Ministry of Finance (MoF) and South Kalimantan Provincial Government. The forum emphasised the importance of implementing OJK Regulation (POJK) Number 12 2024 concerning the Anti-Fraud Strategies (SAF) of Financial Service Institutions (FSIs).

4. OJK reiterated the importance of maintaining the reliability of financial reports and nurturing the use of technology and oversight that considers cultural aspects to improve fraud detection and prevention in the financial services sector (SJK) at the International Conference on Technology, Management and Sustainability (ICTMS) 2025. In addition, OJK also seeks to instil the values of integrity from an early age, while expanding the reach of integrity campaigns to Indonesian students abroad.

5. At the Institute of Indonesian Certified Public Accountants (IAPI) Public Gathering held on 21 June 2025, OJK emphasised the important role played by public accountants in terms of maintaining the quality of financial reports, which includes regulatory compliance in the implementation of OJK Regulation (POJK) Number 9 of 2023 that regulates limitations on assignment periods, the reporting obligations of significant findings to OJK and the independence of public accountants, as well as POJK Number 30 of 2023 concerning the Disclosure of Key Audit Matters (KAM).

Overall, governance activities hosted by OJK as of June 2025 have engaged 14,251 participants, including internal OJK personnel and external stakeholders. Such governance activities are expected to strengthen governance in OJK and the financial services sector.

E. Regulatory Enforcement in the Financial Services Sector and Investigation Progress

Executing the investigation function, as of 30 June 2025, OJK investigators have resolved 149 cases, consisting of 123 cases in the banking industry, five cases in the capital market, financial derivatives and carbon exchange (PMDK) sector and one case involving financing institutions, venture capital firms, microfinance institutions and other financial service institutions (PVML). To date, 127 cases have been court adjudicated, including 115 cases with legally binding rulings (in kracht), one case under appeal and 11 cases in cassation as follows:

No | Stage | Banking | PMDK | PPDP | PVML | TOTAL |

Cases | Cases | Cases | Cases | Cases | ||

1 | Review Process | 6 | 12 | 0 | 3 | 21 |

2 | Preliminary Investigation | 5 | 2 | 2 | 3 | 12 |

3 | Formal Investigation | 7 | 2 | 5 | 0 | 14 |

4 | File Preparation | 7 | 0 | 0 | 1 | 8 |

5 | P-21 | 123 | 5 | 20 | 1 | 149 |

6 | SP3 | 11 | 5 | 5 | 0 | 21 |

7 | Not Escalated to preliminary Investigation | 0 | 0 | 0 | 0 | 0 |

8 | Not Escalated to Formal Investigation | 41 | 39 | 6 | 0 | 86 |

9 | Returned to supervisor after resolution | 23 | 8 | 3 | 0 | 34 |

10 | Handled by other law enforcement agency | 41 | 1 | 4 | 1 | 47 |

11 | Non-financial services sector crime | 0 | 0 | 4 | 0 | 4 |

Total | 264 | 74 | 49 | 9 | 396 | |

| ||||||

1 | In Kracht | 92 | 5 | 17 | 1 | 115 |

2 | Appeal | 0 | 0 | 1 | 0 | 1 |

3 | Cassation | 9 | 0 | 2 | 0 | 11 |

Total |

|

|

|

| 127 | |

To date, OJK investigators have completed case handling and transferred cases to the local District Attorney where the incident occurred for at least five banking debtors.

The imposition of penalties against banking crime represents an extension of the banking legal framework in accordance with Act Number 4 of 2023 concerning Financial Sector Development and Strengthening (P2SK Act). Law enforcement is the last resort or final measure that should only be used when other administrative oversight measures are deemed ineffective (ultimum remedium).

Ultimum remedium is one of OJK's commitments when enforcing the law against criminals operating in the financial services sector, which is expected to improve financial sector integrity and help balance financial system stability with efforts to protect customer interests.